small business insurance Florida

Florida Business Insurance and Workers’ Comp Requirements

Florida’s vibrant economy — from tourism and hospitality to construction and healthcare — provides plenty of opportunity for business owners. However, operating a business in the Sunshine State also means meeting specific insurance requirements to stay compliant and protect your company.

Here’s a complete guide to Florida’s business insurance and workers’ comp laws to help you safeguard your operations.

Small Business Insurance Calculator

Get a Business Insurance Quote

Protect your business in minutes. Fast, flexible, affordable coverage from Thimble.

Start Your QuoteInstant quotes. No long forms. No commitment.

Who Needs Business Insurance in Florida?

Nearly all Florida businesses benefit from insurance, regardless of size or industry. While state law does not require general business insurance, certain types are mandatory depending on your operations:

Businesses with employees must carry workers’ compensation insurance.

Businesses that own, lease, or use vehicles for work must have commercial auto insurance.

Healthcare providers (doctors, nurses) must carry medical malpractice insurance.

Contractors and certain licensed professions may be required by local governments or licensing boards to carry specific coverages.

Even if not legally required, business insurance is highly recommended to protect against lawsuits, property damage, employee injuries, and natural disasters common in Florida.

Workers’ Comp: When It’s Required

Florida law requires most employers to carry workers’ compensation insurance:

Construction businesses: Required if you have one or more employees, including owners

Non-construction businesses: Required if you have four or more employees (full-time or part-time), including business owners

Agricultural businesses: Required if you have six or more regular employees, or twelve or more seasonal employees working more than 30 days.

Exemptions: Sole proprietors and partners in non-construction businesses are not considered employees unless they opt in.

Failure to provide workers’ comp can result in severe fines, stop-work orders, and even criminal penalties.

Commercial Auto Insurance Basics

If your Florida business owns, leases, or uses vehicles for business purposes, commercial auto insurance is mandatory:

Minimum required coverage:

$10,000 in Personal Injury Protection (PIP)

$10,000 in Property Damage Liability (PDL)

Higher limits may be required for certain vehicles (e.g., trucks, taxis).

Personal vehicles used for business may not be covered under a personal auto policy; consider hired and non-owned auto insurance (HNOA).

Not carrying required commercial auto insurance can result in fines, license suspension, and other penalties.

Professional Liability for Certain Jobs

Professional liability insurance (also called Errors & Omissions or E&O) is not required for all businesses in Florida, but is mandatory or highly recommended for certain professions:

Required for:

Doctors (medical malpractice): $100,000 per claim/$300,000 annual aggregate.

Some contractors, consultants, and licensed professionals may need it for licensing or contracts.

Recommended for:

Any business providing professional services or advice, such as architects, engineers, accountants, consultants, IT professionals, real estate agents, and more.

Clients or contracts may require proof of professional liability insurance even if the state does not.

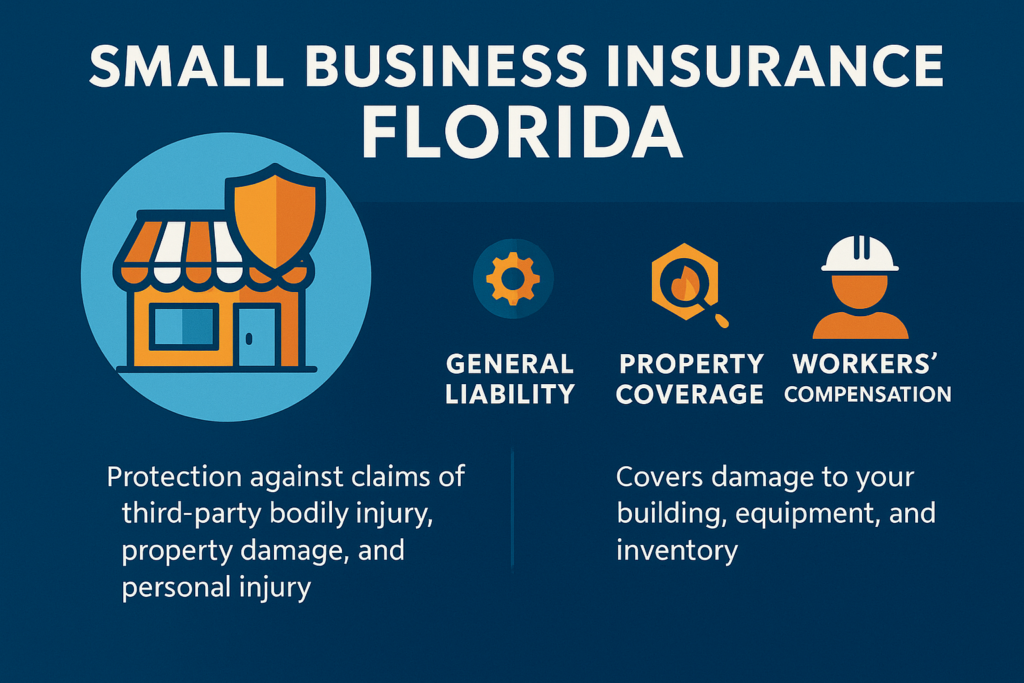

Is General Liability Insurance Mandatory?

General liability insurance is not required by Florida state law for most businesses. However:

It is often required by:

Landlords for commercial leases

Clients or contracts

Local governments or licensing boards (especially for contractors and trades)

Coverage includes:

Third-party bodily injury

Property damage

Personal and advertising injury (e.g., slander, libel)

General liability insurance is highly recommended to protect against common lawsuits and is essential for business credibility.

Other Useful Coverages for Businesses

Florida businesses should consider additional insurance policies to fully protect their operations:

Business Owner’s Policy (BOP): Bundles general liability and property insurance, often at a discount.

Commercial Property Insurance: Protects against fire, theft, hurricanes, and other disasters.

Business Interruption Insurance: Covers lost income if your business is forced to close due to a covered event.

Cyber Liability Insurance: Protects against data breaches and cyberattacks.

Umbrella Insurance: Provides additional liability coverage above your other policies.

Inland Marine Insurance: Covers tools and equipment in transit or at job sites.

Summary Table: Florida Business Insurance Requirements

| Insurance Type | Required? | Who Needs It / When Required | Minimum Limits / Notes |

|---|---|---|---|

| Workers’ Compensation | Yes | Construction: 1+ employees; Non-construction: 4+ | State-regulated |

| Commercial Auto Insurance | Yes (if using vehicles) | Any business using vehicles for work | $10,000 PIP, $10,000 PDL |

| General Liability Insurance | Sometimes (see notes) | Contractors (licensing), leases, some localities | Varies; often required by contracts |

| Professional Liability (E&O) | Sometimes (see notes) | Doctors, some licensed professionals, contracts | $100k/$300k for doctors |

| Business Owner’s Policy (BOP) | No | Recommended for small businesses | Bundles property & liability |

| Commercial Property Insurance | No | Recommended for property owners | - |

| Business Interruption Insurance | No | Recommended for all businesses | - |

| Cyber Liability Insurance | No | Recommended for data-sensitive businesses | - |

| Umbrella Insurance | No | Recommended for added liability protection | - |

In summary: Florida businesses must comply with workers’ comp and commercial auto insurance requirements, while general liability and professional liability insurance are often necessary for contracts, licensing, or risk management. Additional coverages like BOP, property, and cyber insurance help protect against Florida’s unique risks, including hurricanes and litigation. Always check with your local city or county for additional requirements.

Florida Business Insurance: Frequently Asked Questions (FAQs)

Is business insurance required by law in Florida?

Certain types of business insurance are required by Florida law. Workers’ compensation insurance is mandatory for most employers with four or more employees (and for construction businesses with even one employee). Commercial auto insurance is also required if your business owns or uses vehicles for work. General liability insurance is not required by state law but may be required by local governments, landlords, or clients.

What does Florida business insurance typically cover?

Business insurance in Florida can cover property damage, liability claims, employee injuries, business interruption, and cyber threats. Common policies include general liability, commercial property, workers’ compensation, commercial auto, and professional liability insurance.

Who needs workers’ compensation insurance in Florida?

Construction businesses: Required if you have one or more employees, including owners.

Non-construction businesses: Required if you have four or more employees, including owners.

Agricultural businesses: Required if you have six or more regular employees or twelve or more seasonal employees working more than 30 days.

Is general liability insurance mandatory for Florida businesses?

No, general liability insurance is not required by state law. However, it is highly recommended and often required by landlords, clients, or for certain licenses. Some cities and counties may have their own requirements, so always check with local authorities.

What are the commercial auto insurance requirements in Florida?

If your business owns, leases, or uses vehicles for business purposes, you must have commercial auto insurance. The minimum required coverage is $10,000 in personal injury protection (PIP) and $10,000 in property damage liability (PDL). Higher limits may be required for certain vehicles or industries.

Do I need professional liability insurance in Florida?

Professional liability insurance is not required for most businesses, but it is mandatory for doctors (medical malpractice insurance) and may be required for other licensed professionals or by contract. Many service-based businesses choose this coverage to protect against lawsuits over errors or negligence.

How much does business insurance cost in Florida?

Costs vary based on business size, industry risk, location, and coverage limits. On average, Florida small businesses pay between $500 and $5,000 annually. Businesses in hurricane-prone areas or high-risk industries may pay more.

Can I bundle business insurance policies to save money?

Yes, bundling policies—such as through a Business Owner’s Policy (BOP) combining general liability and property insurance—can provide comprehensive coverage at a lower cost.

What happens if I don’t have required business insurance?

Operating without required insurance exposes your business to significant financial risks, potential lawsuits, fines, and loss of business opportunities. For example, not carrying workers’ comp or commercial auto insurance can result in severe penalties.

Are business insurance premiums tax-deductible in Florida?

Yes, premiums for policies that protect your business (like general liability, property, and workers’ compensation) are generally tax-deductible as ordinary and necessary business expenses. Consult a tax professional for details.

Does business insurance cover hurricane or flood damage?

Commercial property insurance typically covers hurricane wind damage, but flood damage usually requires a separate flood insurance policy. Review your policy to ensure you have the right protection for Florida’s weather risks.

How do I get a certificate of insurance for my business?

Once you purchase a policy, your insurance provider can issue a certificate of insurance as proof of coverage. This is often needed for contracts, leases, or licensing.

Share This

Customer Reviews

Blake Insurance Group

Phone: (888) 387-3687

Email: info@blakeinsurancegroup.com

Hours: Mon-Fri 9:00 am to 5:00 pm

Sat-Sun: Closed

Blake Nwosu

Owner & Principal Agent

Expertise: All personal and commercial line insurance, including auto, home, business, health, and life insurance.

License: 16117464