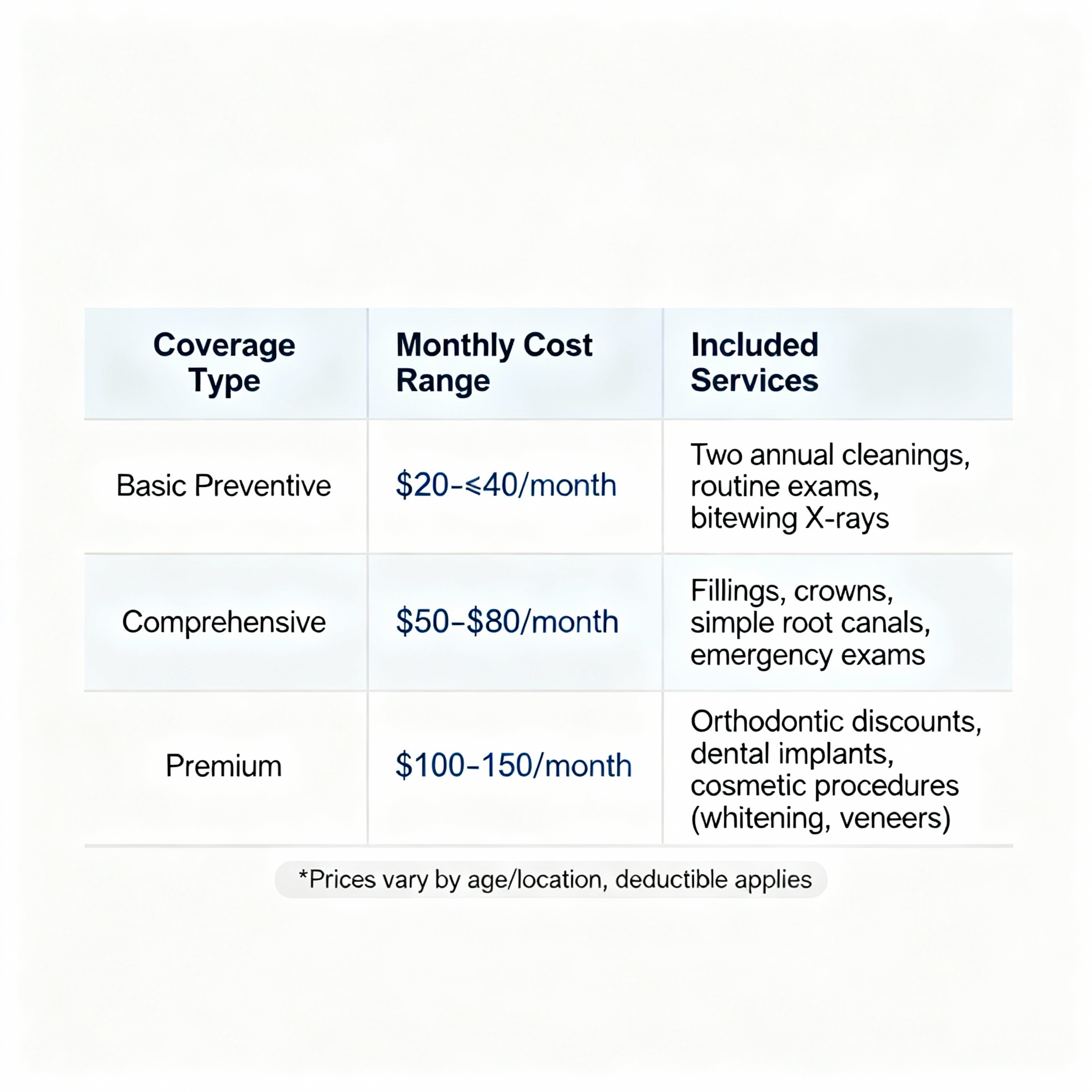

How Much Is Dental Insurance in 2026? Realistic Monthly Costs, What Changes the Price, and How to Compare Real Value

Searching for dental insurance near me usually starts with one question: “How much is it per month?” That matters, but premium alone does not tell you whether the plan is actually a good deal. The better question is how the plan performs over a full year after cleanings, exams, X-rays, fillings, possible crowns, waiting periods, annual maximums, and network rules are all included. In 2026, the plan that looks cheapest each month is not always the plan that leaves you with the lowest dental bill by year-end.

The strongest dental plan is the one that matches how you actually use the dentist. If you mostly want predictable preventive care and a lower monthly cost, a leaner plan can be enough. If you expect basic work, a crown, periodontal treatment, or possible implant-related expenses, richer benefits and a better annual maximum may be worth paying for. The clean way to shop is to compare the plan type, the network, the waiting periods, and the likely 12-month out-of-pocket cost on the same baseline instead of focusing on premium alone.

How much does dental insurance usually cost in 2026?

For many shoppers, individual dental plans generally fall into two broad price lanes. Lower-cost HMO or DMO-style plans often come in at the bottom of the monthly range and use fixed copays with a required network dentist. PPO plans usually cost more each month, but they tend to give you broader dentist choice, more flexible access, and a structure that feels more familiar to buyers who want to keep a current dentist. Richer PPOs can also add stronger major-service percentages, shorter waiting periods, and higher annual maximums, which is why their premiums run higher.

| Plan style | Typical monthly range | Why it may cost more or less | Best fit |

|---|---|---|---|

| Low-cost HMO / DMO | Usually the lowest monthly range | Lower premium in exchange for fixed network use and less flexibility | Shoppers who are comfortable using a network dentist and want predictable routine care |

| Budget PPO | Low-to-mid monthly range | More flexibility than HMO/DMO, but often with waiting periods and a modest annual maximum | People who want choice but do not need top-tier major coverage |

| Richer PPO | Mid-to-higher monthly range | Higher annual maximums, better major coverage, or shorter waits can raise premium | Households expecting heavier use or who want stronger protection against costly work |

| Family dental plans | Higher than individual pricing and tied to member ages and count | More covered lives and more expected use usually lift total premium | Families trying to balance preventive care, pediatric needs, and occasional restorative work |

How to compare dental insurance so the winner is real

Most weak dental-plan decisions happen because buyers compare premium only. That misses the features that actually control value. Waiting periods, annual maximums, preventive coverage, network rules, and how the plan treats basic versus major services are usually more important than saving a few dollars a month on premium.

- Start with your dentist: decide whether keeping your current dentist matters or whether you are open to switching.

- Estimate your likely use: preventive only, preventive plus fillings, or possible crowns, perio, or more complex work.

- Check waiting periods: a low premium can be less valuable if the service you need is not available soon enough.

- Look at annual maximums: richer plans can be worth it when higher-cost work is likely.

- Use one-year math: compare premium plus expected out-of-pocket instead of premium alone.

Dental plan styles — budget vs richer coverage, PPO vs HMO/DMO

The chart below is the easiest way to shortlist plans before you quote. It helps separate flexibility buyers from savings buyers.

| Category | Budget PPO Dental | Low-Cost HMO/DMO Dental |

|---|---|---|

| Typical monthly cost | Usually higher than HMO/DMO, but still a value choice for flexibility | Usually the lowest monthly premium lane |

| Network / access | Broader dentist choice and more flexibility | Must use the plan’s contracted dentist network |

| Coverage structure | Percent-based benefits are common for basic and major work | Copay-based design is common for routine and restorative services |

| Waiting periods | Often more likely on basic and major services | Can be lighter on routine access, but depends on exact plan |

| Best fit | People who want to keep dentist choice open | Shoppers who care most about minimizing monthly cost and accept network restrictions |

What actually changes your dental insurance price

Premium moves when certain benefit choices improve. That does not mean the higher-priced plan is overpriced. It means the plan is offering more somewhere, and the only question is whether your household is likely to use that difference.

| Factor | How it changes price | Smart move |

|---|---|---|

| Network type | PPO usually costs more than HMO/DMO because flexibility is broader | Pay for PPO only if provider flexibility matters to you |

| Annual maximum | Higher maximums usually push premium higher | Choose a richer max only if you may use more than routine care |

| Waiting periods | No-wait or shorter-wait plans often cost more | If work is likely soon, paying more for faster access can be worth it |

| Major-service strength | Better crown, bridge, denture, or other major coverage raises cost | Buy richer major coverage when those services are realistically on the horizon |

| Implant / ortho features | Extra specialty richness can increase premium materially | Only pay for these if someone in the household may truly use them |

| Family composition | More members and pediatric use generally increase total premium | Compare family plans using total household value, not just individual plan logic |

Which plan type tends to fit which usage pattern?

The easiest way to avoid overpaying is to match the plan to your most likely year, not your most optimistic month.

| Usage pattern | Usually strongest fit | Why |

|---|---|---|

| Mostly preventive only | Low-cost HMO/DMO or lean PPO | Routine care can be handled efficiently without paying for rich major benefits you may not use |

| Preventive plus occasional fillings | Budget PPO or strong low-cost HMO/DMO | Basic service value starts to matter, but top-tier richness may still be unnecessary |

| Possible crown or heavier restorative year | Richer PPO with better major-service support | Higher annual maximum and better major coverage can justify the extra premium |

| Keeping a specific dentist matters | PPO | Flexibility and continuity usually matter more than shaving a few dollars off monthly premium |

| Open to switching dentists for savings | HMO/DMO | That willingness often unlocks the lowest-cost path to ongoing routine care |

Dental insurance “near me” — networks, ZIP code fit, and where we help

Dental shopping is local. The same carrier can look much stronger in one ZIP code than another because dentist participation, appointment access, and plan availability vary. The best process is to confirm whether your preferred practice is in-network first, then compare waiting periods and annual maximums on the plans that actually work in your area.

| Region block | States | Common shopping note |

|---|---|---|

| West & Southwest | AZ, CA, NM, TX | Provider verification matters because metro and rural access can differ sharply by ZIP |

| South & Southeast | AL, FL, GA, NC, SC, VA | Compare preventive value, waiting periods, and family pricing together |

| Midwest & Plains | IA, KS, MI, NE, OH, OK, SD | PPO versus HMO tradeoffs often come down to dentist choice and local network density |

| Northeast & East | NY, WV | Richer PPO value can matter more when specialist or provider continuity is important |

Get personalized, budget-friendly dental quotes

Start with the quote path that matches how you want to shop. If you want a direct dental-and-vision shopping path, use the Ameritas option below. If you want to review additional under-65 individual options, use the second quote path. The best result comes from checking your dentist, household members, expected procedures, and whether vision should be bundled before you enroll.

Use your ZIP code, dentist preference, and likely dental work as the baseline when you compare plans.

Frequently asked questions

Is dental insurance worth it if I mostly get cleanings?

Usually yes. A preventive-first plan can pay back quickly through cleanings, exams, and routine X-rays while also reducing the chance that delayed care turns into more expensive work later.

Which is usually cheaper: PPO or HMO/DMO?

HMO or DMO plans are usually cheaper monthly, but they require you to use a contracted dentist. PPO plans usually cost more because they offer more flexibility and broader choice.

Can I get dental insurance with no waiting period?

Preventive care is often available right away, but no-wait access to basic or major work is less common and usually costs more. If treatment is likely soon, waiting-period rules deserve extra attention before you buy.

Do plans usually cover implants or orthodontics?

Some plans do, but those benefits often come with tighter rules, waiting periods, missing-tooth clauses, age limits, or lifetime maximums. Those details should be verified before paying extra for richer coverage.

How do I avoid surprise dental bills?

Confirm your dentist’s network status, review waiting periods, check the annual maximum, and request a treatment estimate for expensive work. Those four steps catch many of the surprises buyers run into later.

Related topics

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Availability, networks, waiting periods, annual maximums, and covered services vary by carrier, ZIP code, and plan design. Review policy documents for exact terms, exclusions, and limitations.

Marketplace note: Pediatric dental must be available through Marketplace coverage, while adult dental is generally not an essential health benefit and is typically purchased separately or through optional benefit designs.

Reviews are loaded from Google when you click “View reviews.”