Short-Term Health Insurance (2026): Temporary Coverage for Gaps Between Jobs, Missed Enrollment Windows, or Waiting Periods

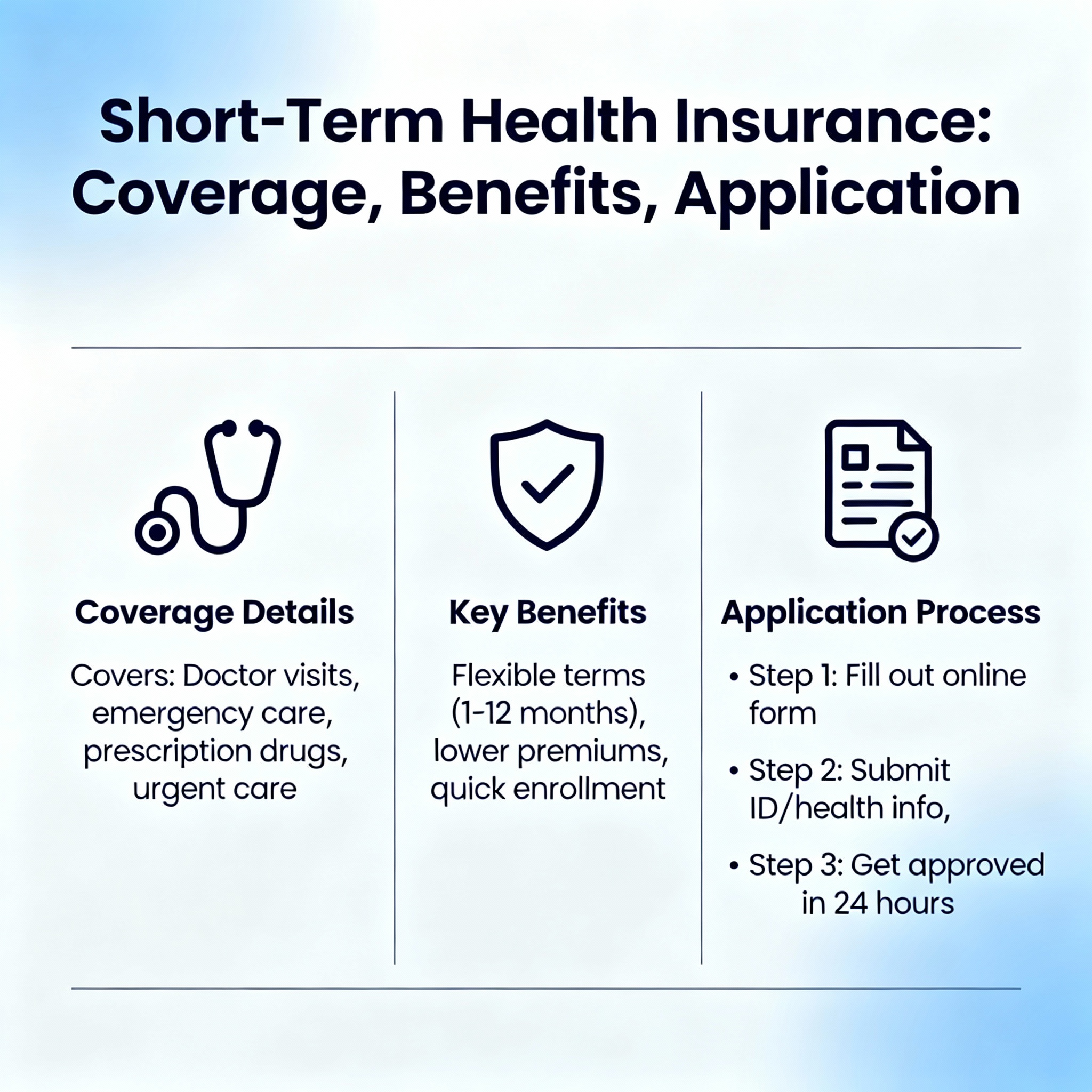

Short-term health insurance is designed for one job: helping healthy applicants cover a temporary gap when they do not have traditional major medical coverage in place. In 2026, that usually means a short bridge between employer plans, a waiting period before new group coverage begins, a missed Marketplace enrollment deadline, or another temporary timing problem. It is built for speed and flexibility, but it is not built to replace Affordable Care Act coverage.

That difference matters. Short-term medical plans are generally medically underwritten, can exclude pre-existing conditions, and do not have to cover the full package of essential health benefits required of ACA Marketplace plans. They can still be useful in the right situation, especially when the goal is protection from large, unexpected bills tied to a sudden illness or injury. But they should be selected with clear expectations. This is gap coverage, not comprehensive long-term protection.

For coverage periods beginning on or after September 1, 2024, the federal definition generally limits short-term plans to an initial term of no more than 3 months and a maximum total duration of no more than 4 months, though state rules can be stricter or may prohibit these plans altogether.

If you are searching for short-term health insurance near me, the first step is always to confirm whether your state allows these plans and how long they can last where you live.

Short-term plan snapshot

The right way to shop short-term coverage is to start with its role. It is temporary coverage for a defined gap. It is usually not the best answer for people who need ongoing prescription coverage, predictable long-term renewals, guaranteed acceptance, maternity care, or strong pre-existing condition protection. It can work best when you need fast enrollment, understand the limitations, and mainly want a financial buffer against a large covered medical bill during a short transition period.

| Item | What to expect |

|---|---|

| Primary purpose | Temporary coverage for a short gap between other health plans |

| Enrollment timing | Often available year-round, subject to carrier and state rules |

| Pre-existing conditions | Generally excluded or limited |

| Best use case | Healthy applicants who need quick gap coverage and understand the trade-offs |

Short-term health insurance vs ACA Marketplace plans

This is the comparison that matters most. ACA plans are comprehensive individual health insurance coverage. They cover essential health benefits, cannot deny you for pre-existing conditions, and may come with premium tax credits and cost-sharing reductions if you qualify. Short-term plans are different by design. They are temporary, limited, and generally cheaper for healthy applicants because they cover less and underwrite more.

| Feature | Short-term health insurance | ACA Marketplace plan |

|---|---|---|

| Enrollment | Often any time, subject to carrier and state rules | Open Enrollment or Special Enrollment Periods |

| Pre-existing conditions | Usually excluded or restricted | Covered with no health underwriting |

| Essential health benefits | Often limited and policy-specific | Comprehensive coverage required |

| Subsidies | Not subsidy-eligible | May qualify for premium tax credits and other savings |

| Duration | Temporary and heavily state-dependent | Full policy year with annual renewal structure |

| Typical buyer | Healthy applicant solving a short timing problem | Anyone seeking comprehensive major medical coverage |

Who short-term health insurance may fit—and who should usually choose ACA instead

| Situation | Why it may fit | When ACA is usually better |

|---|---|---|

| Between jobs | You need a short bridge before new benefits begin | If you need stronger benefits or have ongoing conditions |

| Missed Open Enrollment | You need temporary protection while waiting for the next ACA window | If you qualify for a Special Enrollment Period now |

| Recent graduate or transitional period | You want fast, stopgap coverage during a short changeover | If you want long-term predictable coverage |

| Healthy applicant focused on catastrophic-style risk | You mainly want help with large unexpected covered bills | If you need prescriptions, maternity, mental health, or pre-existing condition protection |

Costs, deductibles, and what drives the price

Short-term premiums are often lower than ACA plan premiums before subsidies, but that does not automatically make them the better value. Price is shaped by age, location, tobacco use, deductible choice, coinsurance design, benefit maximums, optional riders, and state rules. Lower premiums usually come with higher deductibles or narrower benefits. That means the real question is not just what you pay each month. It is what you are exposed to if you actually use the policy.

| Cost factor | Why it changes price | Smart buying approach |

|---|---|---|

| Deductible | Higher deductibles usually reduce the monthly premium | Pick a deductible you could realistically cover from savings |

| Term length | Longer approved coverage periods can cost more where allowed | Buy only the amount of time you truly need |

| Benefit structure | Coinsurance, caps, and plan design affect both premium and exposure | Review the certificate before treating it like major medical |

| Optional riders | Added features can increase total premium | Only add extras that solve a real gap for you |

States and cities where shoppers often look for short-term health quotes

State regulation drives availability. Some states permit short-term plans with tight limits, some are stricter than federal rules, and some effectively do not allow them. That is why location always comes first when comparing options.

| State | Example cities | Shopping note |

|---|---|---|

| Arizona | Phoenix, Tucson, Mesa, Chandler | Availability and term rules can vary by ZIP and carrier |

| Texas | Houston, Dallas, San Antonio, Austin | Check deductible and network trade-offs closely |

| Florida | Miami, Orlando, Tampa, Jacksonville | Compare short-term against ACA subsidy eligibility before deciding |

| North Carolina | Charlotte, Raleigh, Greensboro, Durham | Review state-specific duration and carrier availability |

Get short-term health insurance quotes now

The cleanest way to shop is to compare temporary plan options against your actual gap length, deductible comfort level, and backup options such as ACA coverage or upcoming employer benefits. If you may qualify for a Special Enrollment Period or premium assistance through the Marketplace, compare that first before relying on a temporary plan.

Temporary coverage can be useful when the fit is right. It should never be confused with comprehensive ACA major medical coverage.

Short-term health insurance FAQs (2026)

How fast can short-term coverage start?

Some short-term policies can begin quickly after approval, depending on the carrier, state, and the effective date you choose.

Are pre-existing conditions covered?

Usually not. Short-term plans commonly exclude or limit pre-existing conditions, so review the policy language carefully before enrolling.

Does short-term coverage include all ACA benefits?

No. Short-term plans are not required to cover the full set of essential health benefits that ACA Marketplace plans must include.

Can I get subsidies for short-term health insurance?

No. Premium tax credits and cost-sharing reductions apply to qualifying ACA Marketplace coverage, not short-term medical plans.

What should I check before buying a short-term plan?

Confirm state availability, deductible, coinsurance, exclusions, network rules, benefit caps, term length, and whether you might qualify for ACA coverage instead.

Related topics

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Short-term health insurance is not ACA-compliant major medical coverage. It may exclude pre-existing conditions and may not cover all essential health benefits. Availability, underwriting, duration, benefits, limitations, renewals, and exclusions vary by state and carrier. Review the policy or certificate carefully before enrolling.

Trademarks: Carrier and platform names are trademarks™ or registered® trademarks of their respective owners. Use of them does not imply affiliation or endorsement.