Final Expense Insurance in Florida & California (2026): Simple Coverage, Predictable Premiums, Clear Plan Types

If you’re searching for a licensed agent near me to help with final expense coverage, you’re usually trying to solve one problem: make sure your family isn’t forced to fund funeral and end-of-life costs on short notice. Final expense insurance is designed for speed, simplicity, and predictable monthly premiums—so beneficiaries can handle immediate expenses without draining savings or taking on debt.

Final expense is typically a form of permanent life insurance (often whole life) with smaller face amounts and simplified underwriting. The goal is not “maximum life insurance”—it’s a practical benefit that covers common costs like funeral home services, cremation or burial, transportation, an obituary, ceremony expenses, and related bills that tend to arrive quickly. Nationally, common planning numbers often fall around $10,000–$25,000, but the right amount depends on your preferences (burial vs. cremation), local prices, and whether you want a cushion for travel, debts, or a small legacy gift. (For context, recent national median figures often cited in the industry are around $8,300 for a funeral with viewing and burial and about $6,280 for viewing and cremation—before many cemetery-related expenses.)

Final expense plan types at a glance

Most shoppers in Florida and California see the same three tiers. The difference is not just “price”—it’s how the benefit is paid during the first 24 months for natural causes and what health questions you’ll answer. We map your situation to the correct tier first, then price it. That’s how you avoid wasted applications and avoidable declines.

Important: “Final expense” is a purpose, not a single policy form. Always confirm the benefit schedule, waiting period terms, and exclusions on the application and the issued policy.

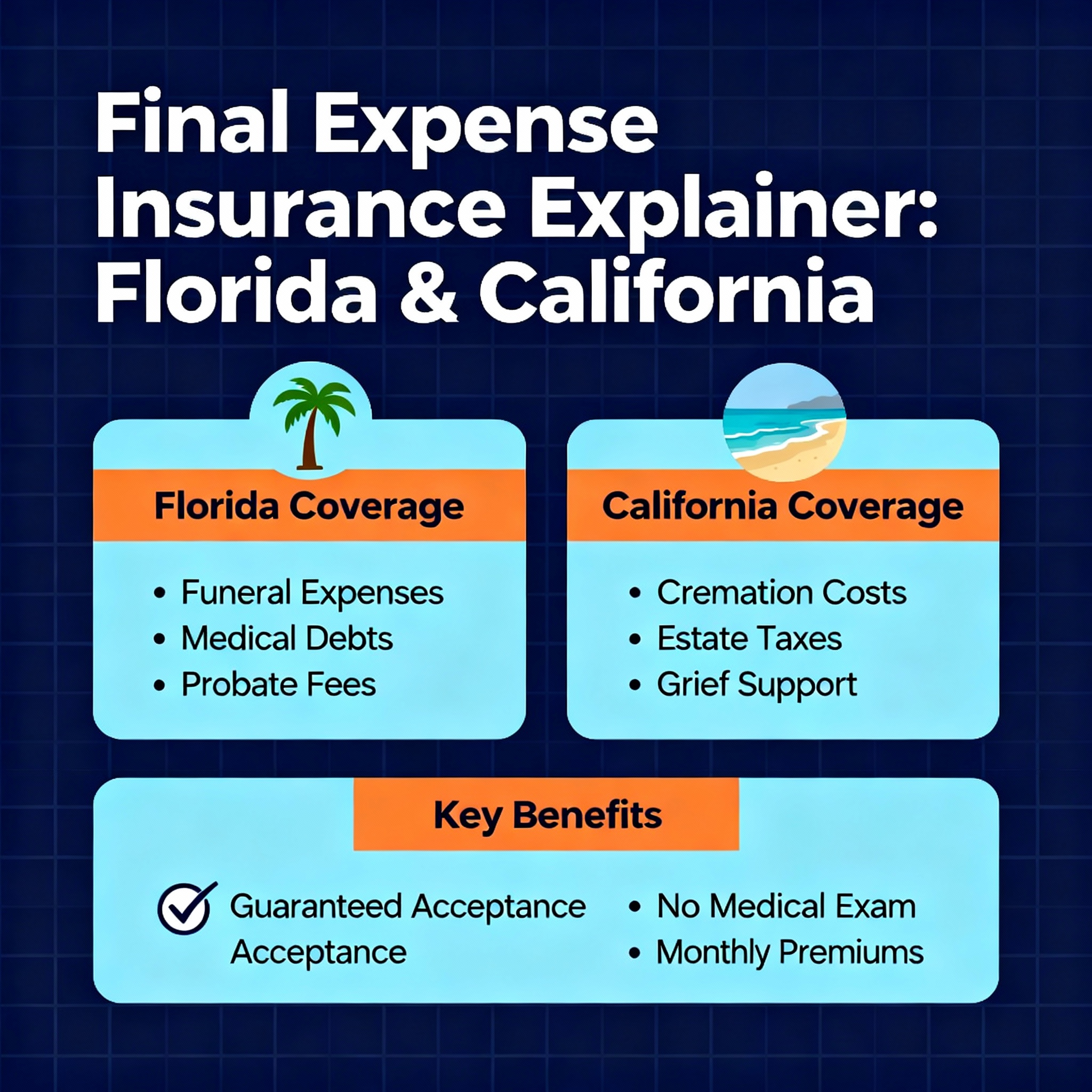

Florida vs. California — side-by-side comparison

Florida and California are both large, highly regulated markets with broad carrier availability. Most differences you’ll feel as a consumer are practical: disclosure steps, plan availability by age band, and which carriers are most competitive for your health profile. The table below is a neutral guide to what we verify so you can avoid “looks good online” quotes that change during underwriting.

| Category | Florida | California | What we verify |

|---|---|---|---|

| Typical face amounts | $5,000–$40,000 across most tiers (age-dependent). | $5,000–$30,000 common; higher bands may tighten by age. | Min/max by age, tobacco class, and tier (level/graded/GI). |

| Issue ages | Commonly mid-40s through mid-80s for simplified issue. | Commonly mid-40s through mid-80s for simplified issue. | Birthday rules (age last vs. nearest) and max age by tier. |

| Waiting period mechanics | Graded/GI often use a 24-month natural-cause limitation. | Graded/GI often use a 24-month natural-cause limitation. | Exact schedule: % payout vs return-of-premium + interest. |

| Underwriting checks | e-App tools, prescription checks, and build charts are common. | Similar checks; extra acknowledgments/disclosures may apply. | Recent hospitalizations, cardiac history, cancer recency, COPD, insulin use. |

| Premium modes | Monthly EFT/debit common; bank draft often preferred. | Monthly EFT/debit common; bank draft often preferred. | Fees for payment mode, grace period, reinstatement rules. |

| Riders & extras | Accelerated benefits and accidental death riders are common. | Rider availability can vary more by filing—confirm early. | Which riders are actually issued in your state and at what cost. |

Bottom line: In both states, the “best” plan is the one that matches your health tier and gives your family clear, usable benefits—without surprises during the first two years.

Plan fit guide: pick the right tier first

Most shopping mistakes happen when someone applies for level benefit with a health history that’s likely to land them in graded or GI anyway. A clean strategy is to choose the tier that best matches your situation, then compare carriers inside that tier so you’re not comparing apples to oranges.

| Tier | Who it’s best for | What you get | What to watch |

|---|---|---|---|

| Level benefit | Stable health, routine medications, no major recent hospital events. | Typically full benefit for natural + accidental causes from day one. | Answer accuracy matters—misstatements can cause delays or denial. |

| Graded benefit | Moderate health history or “borderline” conditions. | Limited natural-cause benefit during first 24 months; accidental often 100% day one. | Know the schedule. Some plans pay % of face; others refund premium + interest early. |

| Guaranteed issue | Recent or serious conditions where simplified issue is unlikely. | No health questions; predictable issue if age-eligible. | Two-year natural-cause limitation is common; confirm benefit math and effective date. |

Costs & rate drivers: what actually determines price

Final expense premiums are designed to be level, but your initial rate depends on a few predictable levers. The fastest way to keep costs reasonable is to match your tier correctly and avoid unnecessary rider add-ons. We also keep the “inputs” clean so carriers don’t re-rate after prescription checks or build verification.

| Driver | Why it matters | What to do |

|---|---|---|

| Age & tobacco | Age is the biggest lever; tobacco classes rate higher. | Apply sooner; disclose accurately; if you’ve quit, confirm the carrier’s tobacco-free timeframe. |

| Health history | Recent cardiac events, cancer recency, COPD, oxygen, insulin use can shift tiers. | Pre-screen before applying; target the right tier to avoid declines and delays. |

| Face amount | Higher coverage increases premium, but cost per $1,000 can improve. | Right-size to your plan (burial vs cremation, travel, family support). |

| Payment method | Some carriers prefer EFT and may price or process more favorably. | Use bank draft where possible; confirm grace periods and reinstatement rules. |

| Riders | Riders can add value but raise cost; availability varies by state filing. | Add only what you need; verify rider availability and cost in FL vs CA before e-sign. |

Pro move: ask for a “clean compare” with the same face amount and the same tier across carriers. That’s how you see true value—not just marketing.

Pro tips before you apply (to prevent surprises)

Final expense is meant to be simple, but the application details still matter. A few minutes of preparation prevents re-quotes, prevents mismatched tiers, and keeps your family’s benefit usable when it matters.

- Decide the amount first: list the service you want, likely totals, and whether you want a cushion for travel or small debts.

- Know your medications: have names and dosages ready—prescription checks can change tier placement if information is incomplete.

- Understand the first 24 months: ask whether early natural-cause benefits are a % schedule or return-of-premium + interest, and how accidental death is handled.

- Set beneficiaries carefully: confirm spelling, relationship, and contingent beneficiaries to reduce claim delays.

- Pick a stable draft date: align payments with income timing to avoid lapses (Social Security, pension, or payday).

- Know what this is not: final expense typically isn’t designed to replace income for decades; it’s focused on immediate costs and predictable premiums.

Timing note: approvals can be quick with e-application workflows, but the actual effective date depends on carrier rules and successful initial payment. Your issued policy controls all benefits and limitations.

Service areas: Florida & California metro support

We help shoppers across major metros in Florida and California. If you’re relocating between states or coordinating coverage for parents in another city, tell us—ZIP code and tobacco status are two of the fastest inputs to get accurate pricing.

| Florida metros | California metros | What we help you confirm |

|---|---|---|

| Miami, Fort Lauderdale, West Palm Beach, Tampa, Orlando, Jacksonville, Tallahassee | Los Angeles, San Diego, San Jose, San Francisco, Sacramento, Fresno, Riverside, Oakland | Tier fit (level/graded/GI), benefit schedule, beneficiary setup, and payment stability |

If your city isn’t listed, that’s fine—start with your ZIP and we’ll route the quote correctly.

Final expense insurance FAQs for Florida & California (2026)

How much final expense coverage should I buy?

Many families start by pricing $10,000–$25,000 because it often matches typical funeral and immediate expenses. We’ll price multiple amounts so you can balance premium and your goals.

What’s the difference between level benefit, graded benefit, and guaranteed issue?

Level benefit (simplified issue) generally pays the full benefit for natural and accidental causes right away if approved. Graded benefit limits natural-cause benefits during the first 24 months using a schedule that varies by policy, while accidental death is often covered at 100% from day one. Guaranteed issue has no health questions and commonly limits natural-cause benefits for the first two years (often return-of-premium plus interest or a graded percentage), then pays the full benefit after the waiting period.

Will my premium ever increase?

Most final expense whole life policies are designed with level premiums that do not increase due to age. Confirm “level premium” and the exact policy class on the application and the issued policy.

Can I qualify with health conditions?

Yes—options exist for many conditions. Depending on recency and severity, you may be best matched to graded benefit or guaranteed issue. Pre-screening helps avoid declines and reduces turnaround time.

How fast can coverage start?

Approvals can be fast with e-application workflows, but the effective date depends on carrier rules and successful initial payment. Waiting periods—when they apply—are measured from the effective date shown on your issued policy.

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Eligibility, underwriting, policy forms, exclusions, graded/guaranteed benefit schedules, and pricing vary by insurer and state. Your issued policy governs benefits and limitations. This page is general information, not legal or tax advice.

Trademarks: All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply affiliation or endorsement.

Reviews are loaded from Google when you click “View reviews.”