Life Insurance for Diabetics — Rates, Approval Paths & Underwriting Tips

Shopping for life insurance for diabetics doesn’t have to be guesswork. Carriers evaluate similar factors—age at diagnosis, A1C trend, medications, build, and any complications—to decide whether you qualify for simplified issue, no-exam term, or fully underwritten coverage. On this page you’ll find a neutral overview of how insurers usually assess risk, the products that fit Type 1 and Type 2 needs, and practical steps to keep premiums predictable. If you want a licensed agent “near me” to pre-screen your health profile and match you to the right approval path, start with the secure link below.

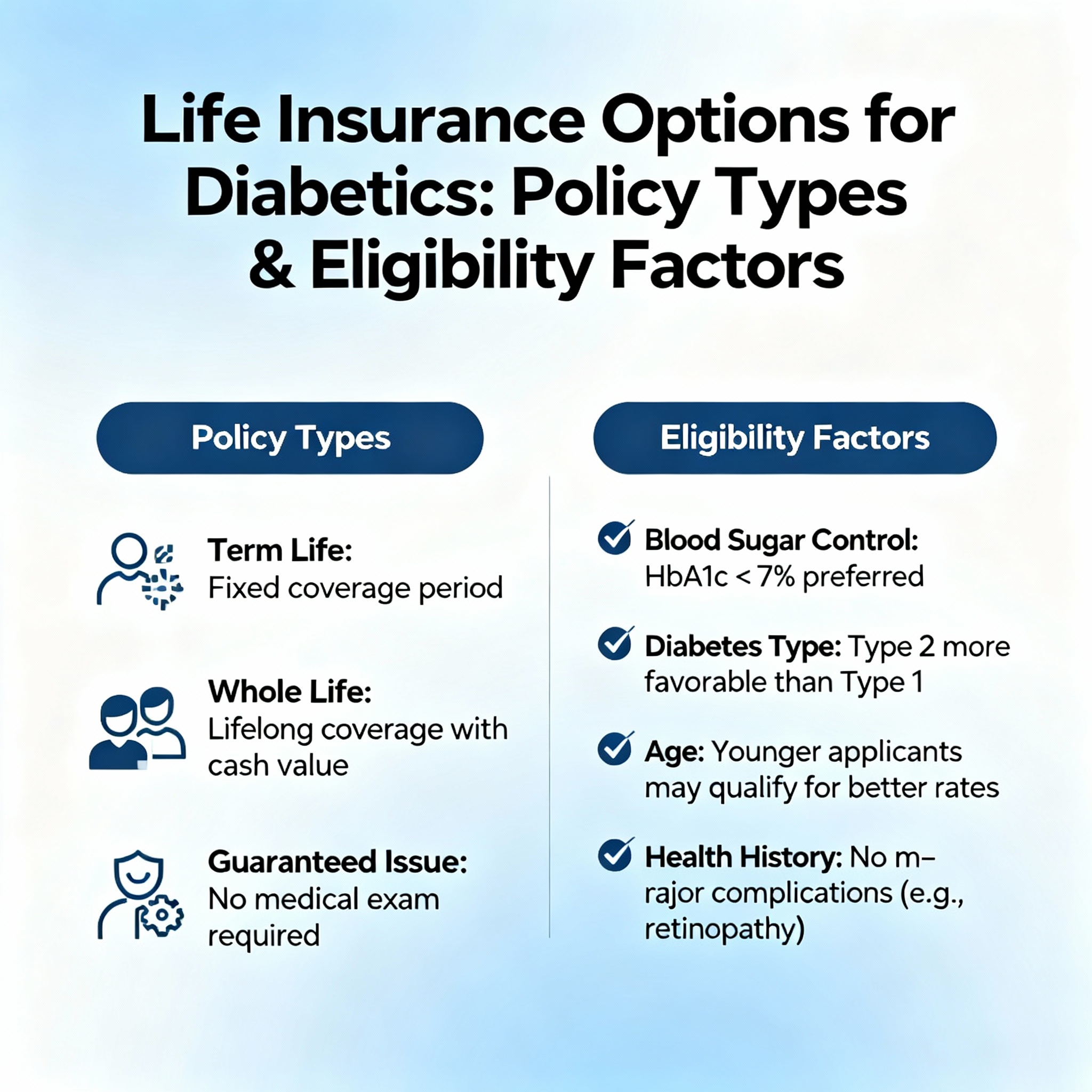

Best-fit policy types for people living with diabetes

No-exam term (simplified issue)

Streamlined health questions and database checks (prescriptions/MIB) instead of a paramedical exam. Good match for well-managed Type 2 and select Type 1 profiles seeking budget-friendly temporary coverage (10–30 years).

Fully underwritten term

Includes labs and vitals; can yield stronger rates for applicants with stable A1C, consistent follow-ups, and no diabetes complications. Useful for higher face amounts or precise pricing.

Whole life / final expense

Permanent coverage with level premiums. Options range from simplified issue (with health questions) to guaranteed issue (no questions; graded benefits in first two policy years). Ideal for lifelong protection and burial costs.

Riders & living benefits

Accelerated death benefit, chronic/critical illness, and waiver-of-premium riders vary by carrier and state. Verify availability with your agent before you apply.

Life insurance options for diabetics — side-by-side

Rules vary by carrier and state filing. Your issued policy controls benefits, limitations, and exclusions.

| Category | No-Exam Term | Fully Underwritten Term | Whole Life / Final Expense | What to verify |

|---|---|---|---|---|

| Typical face amounts | $50k–$500k (varies by age/answers) | $100k–$2M+ (subject to labs/financials) | $5k–$40k common (higher possible) | Minimum/maximum by age, med history, and income |

| Speed | Fast decisions (minutes to days) | Longer (labs/APS may be requested) | Fast; GI is typically instant issue | Any exam/APS triggers; e-sign process |

| Health screening | Questions + data checks, no labs | Questions + labs/vitals (A1C, build) | Questions or none (GI) | Cutoffs for A1C, build, insulin use, complications |

| Best for | Well-managed Type 2; select Type 1 | Strong control and clean follow-ups | Lifelong needs, burial costs, GI scenarios | Rider availability and state-specific rules |

| Premium stability | Level for chosen term | Level for chosen term | Level for life (if designed so) | Ensure level-premium language is in contract |

Pricing drivers & eligibility—how carriers evaluate diabetes risk

Underwriting looks at overall control and stability. Use the matrix below to set expectations and improve placement.

| Driver | Why it matters | What to do |

|---|---|---|

| A1C level & trend | Recent, stable results support better tiers than erratic swings. | Have your latest labs handy; show consistent follow-up visits. |

| Age at diagnosis & duration | Earlier onset or long duration may require more documentation. | Share diagnosis year and treatment milestones with dates. |

| Treatment type | Insulin vs. oral meds vs. lifestyle-only affects risk class. | List medications/dosages and any recent changes. |

| Complications & comorbidities | Neuropathy, retinopathy, kidney or cardiovascular issues impact eligibility. | Provide physician notes when available; we can pre-screen anonymously. |

| Build & tobacco | Height/weight and nicotine use strongly influence premiums. | Share accurate build; consider tobacco-free timelines if applicable. |

| Coverage amount & product | Higher face amounts and permanent plans price differently. | Right-size face amounts to goals; compare term vs. whole lifetime needs. |

Pro tips before you apply

- Pre-screen first: We can review your profile anonymously to target carriers most receptive to your health history.

- Know your numbers: Keep the most recent A1C date/result, diagnosis year, and medications list handy for the application.

- Avoid quick changes: If a medication was just added or adjusted, ask whether to stabilize before applying.

- Right-size the face amount: Match coverage to mortgage balance, income replacement, or final expenses so you don’t overpay.

- Consider riders carefully: Add only benefits you’re likely to use; rider availability differs by state and filing.

Service areas & licensing

| Target Cities | Licensed States |

|---|---|

| Phoenix, Tucson, Mesa, Chandler, Scottsdale, Glendale, Tempe, Peoria, Surprise, Flagstaff, Prescott, Yuma, Sierra Vista, Casa Grande, Queen Creek | AZ, AL, TX, CA, NY, OH, FL, NC, VA, GA, OK, NM, IA, KS, MI, NE, SC, SD, WV |

Life Insurance for Diabetics: FAQ

Can people with diabetes get life insurance?

Yes. Options range from simplified no-exam term to fully underwritten term and permanent policies. The best fit depends on overall control, medications, and any complications.

Does A1C affect my rate?

Insurers consider both your most recent A1C and the trend over time. Stable, well-managed results with routine follow-ups generally improve placement.

Is insulin use an automatic decline?

No. Many carriers offer coverage to insulin users; product and price depend on dosage, duration, and any related conditions. Pre-screening helps avoid mismatches.

Do I need a medical exam?

Not always. No-exam options rely on health questions and database checks. For larger face amounts or nuanced pricing, labs may help you qualify for stronger classes.

How fast can I be approved?

Simplified issue can be minutes to days. Fully underwritten cases take longer if labs or medical records are requested. E-applications and e-signatures speed things up.

Independent agency: Blake Insurance Group LLC is an independent agency. We compare multiple life insurance carriers—brand-neutral—to fit your goals and budget.

Brand ownership: All trademarks and service marks belong to their respective owners. Use here is for identification only; no affiliation or endorsement is implied.

Licensing: Licensed insurance producer (NPN 16944666). State availability and underwriting vary; your issued policy governs benefits and limitations. Not financial or medical advice.

Share This

Customer Reviews

Blake Insurance Group

Phone: (888) 387-3687

Email: info@blakeinsurancegroup.com

Hours: Mon-Fri 9:00 am to 5:00 pm

Sat-Sun: Closed

Blake Nwosu

Owner & Principal Agent