Surety Bond Cost Calculator (2026): Estimate Your Bond Premium and Start an Online Quote

Use this working surety bond cost calculator to estimate what a bond may cost before starting your quote. If you are searching for a surety bond calculator near me, the key number is not just the bond amount. Your actual cost is usually a premium percentage of the required bond amount, adjusted by the bond type, credit profile, underwriting, and obligee requirements.

Surety bond pricing is different from standard insurance pricing. A bond is a three-party guarantee between the principal, the obligee, and the surety company. The obligee sets the required bond amount, but that amount is not usually what you pay. You pay the premium charged by the surety to issue the bond. This page gives you a real on-page calculator, common 2026 pricing ranges, bond-type examples, and a direct online quote path through Propeller.

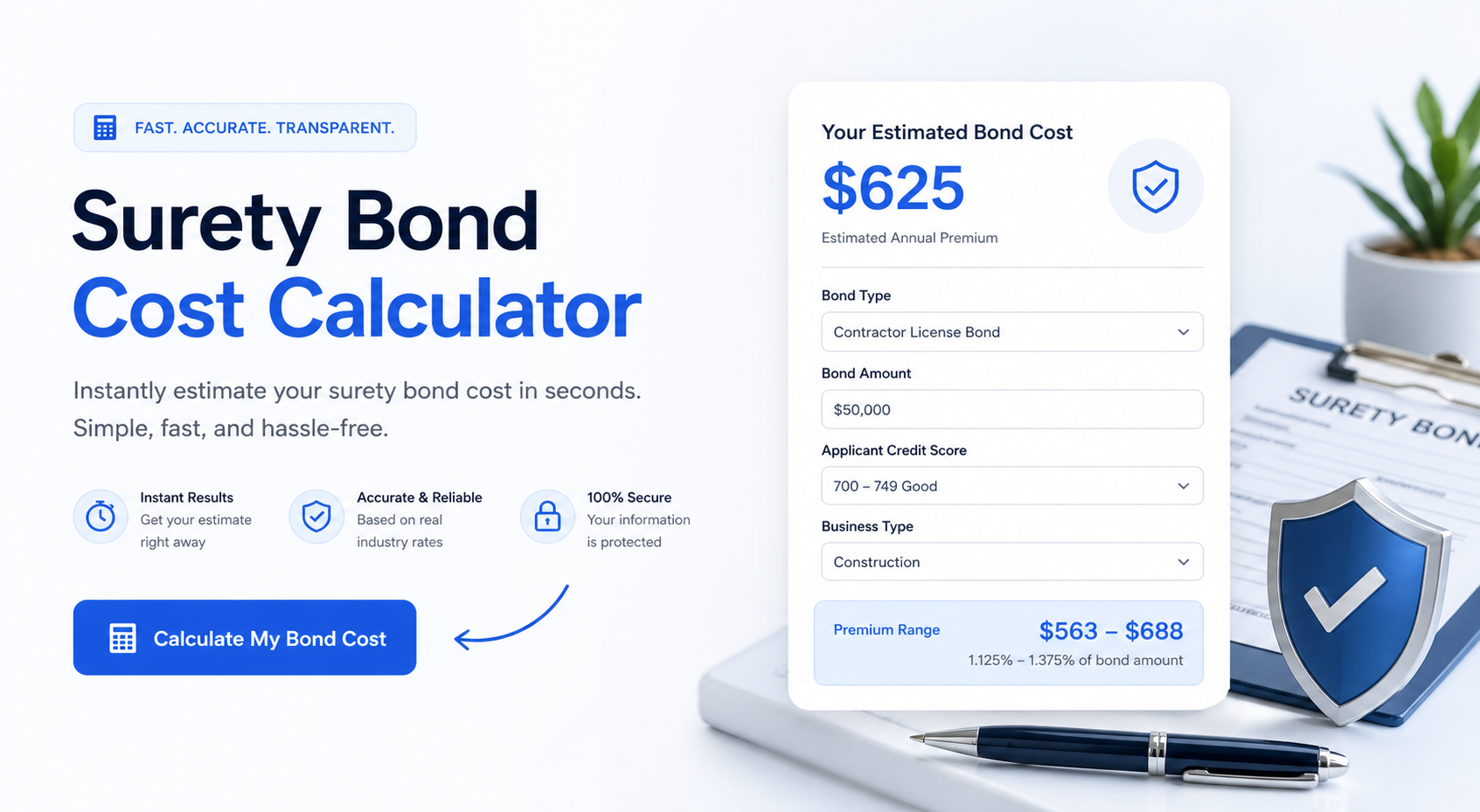

Working surety bond cost calculator

Enter the required bond amount, choose an estimated rate tier, and set the bond term. The calculator estimates the annual premium, term premium, and monthly equivalent. Actual rates depend on the bond type, obligee, underwriting, credit, financials, and surety approval.

Formula used: bond amount × estimated rate tier × term. Many sureties also apply minimum premiums, policy fees, underwriting rules, state-specific requirements, and renewal terms.

How surety bond pricing works

A surety bond premium is usually calculated as a percentage of the required bond amount. For example, a $25,000 bond at a 2% rate estimates to $500 for one year before any minimum premium, fees, taxes, or underwriting adjustments. Some license and permit bonds are simple and fast. Court bonds, contract bonds, fiduciary bonds, and larger commercial surety bonds can require additional documentation.

Typical surety bond cost ranges in 2026

Most commercial surety bonds are priced as a percentage of the bond amount. Low-risk bonds and strong credit profiles often receive lower rates. More complex bonds, larger bond amounts, challenged credit, prior losses, or higher-risk obligations can increase the rate.

| Bond / applicant profile | Common rate range | Example on $25,000 bond | What it usually means |

|---|---|---|---|

| Excellent credit / low-risk bond | 1%–2% | $250–$500 | Clean profile, common bond type, favorable underwriting |

| Standard approval | 2%–4% | $500–$1,000 | Typical small business or license bond profile |

| Moderate underwriting | 4%–7% | $1,000–$1,750 | More review, higher-risk bond type, or mixed credit factors |

| Challenged credit / complex risk | 7%–15%+ | $1,750–$3,750+ | Credit, claims, financials, or bond class requires stronger underwriting |

Common bond types people calculate

The right quote path depends on what type of bond the obligee requires. A contractor license bond is not rated the same way as a probate bond, and a performance bond is not the same as a simple license and permit bond. Use the table below to identify the category before you quote.

| Bond type | Common use | Who requires it | Pricing note |

|---|---|---|---|

| License and permit bond | Business licensing or regulatory compliance | State, city, county, or licensing board | Often fast to quote online |

| Contractor license bond | Contractor licensing and compliance | Contractor boards or local agencies | Credit and license class can matter |

| Notary bond | Notary commission requirement | State agency | Often low-cost and simple |

| Court bond | Probate, fiduciary, appeal, or legal requirement | Court or legal authority | May require underwriting and documentation |

| Performance/payment bond | Contract guarantee for public or private projects | Project owner or general contractor | Financials, capacity, and experience are important |

What affects the final surety bond cost?

The calculator gives a planning estimate. The final quote depends on the exact bond form, obligee requirements, state, applicant credit, business history, prior claims, bond amount, and whether the surety can issue instantly or needs underwriter review. Stronger documentation usually helps the quote process move faster.

| Factor | Why it matters | What to prepare |

|---|---|---|

| Credit profile | Surety bonds rely heavily on applicant responsibility and repayment ability | Owner information and accurate legal name |

| Bond form | Some obligee forms create more risk for the surety | Required bond form or obligee instructions |

| Bond amount | Larger bond amounts can require deeper underwriting | Exact amount required by the obligee |

| Business history | Experience can improve approval strength | Years in business, licenses, project history |

| Claims or cancellations | Prior issues can affect eligibility and rate | Explanation and supporting documentation |

Start your online surety bond quote

After estimating your cost, open the secure online quote tool to get actual bond pricing. Have the required bond amount, obligee name, bond form, business legal name, owner information, and desired effective date ready. The calculator is for planning only; the online quote provides the real underwriting path.

No iframe is embedded on this page. The button opens the external quote tool directly.

Related topics

Surety bond cost calculator FAQs (2026)

Is the bond amount the same as what I pay?

No. The bond amount is the required guarantee amount. Your cost is usually a percentage of that bond amount, subject to minimum premiums, fees, and underwriting.

Can I buy a surety bond online?

Many common commercial surety bonds can be quoted and purchased online. Some court, contract, fiduciary, or complex bonds may require underwriter review.

Why did my final quote differ from the calculator?

The calculator uses estimated rates. Final pricing depends on the exact bond form, obligee, credit, bond amount, state, term, underwriting, and minimum premium rules.

What information do I need for a bond quote?

You typically need the bond amount, obligee name, required bond form, business name, owner information, address, effective date, and sometimes financial or license details.

Does credit affect surety bond cost?

Often, yes. Many commercial surety bonds use credit and underwriting factors to determine approval and rate, especially for larger or higher-risk bonds.

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single surety company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Calculator results are estimates only. Actual bond pricing, eligibility, underwriting requirements, fees, terms, and issuance depend on the surety company, obligee, bond form, state, applicant profile, and final approval.

Trademarks: All product and company names are trademarks™ or registered® trademarks of their respective holders. Use of them does not imply affiliation or endorsement.