Why Homeowners Are Switching from NFIP to Neptune Flood in 2026

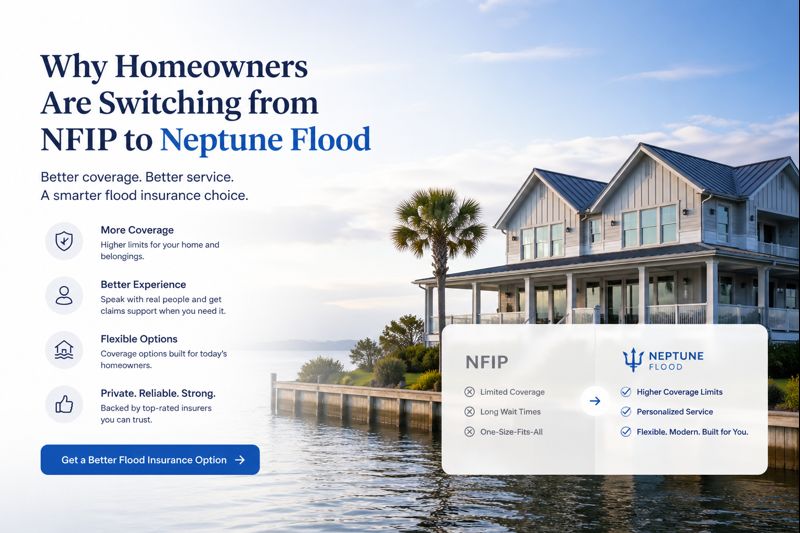

Homeowners are comparing the National Flood Insurance Program (NFIP) with private flood insurance options like Neptune Flood because flood risk, home values, and insurance expectations have changed. In 2026, property owners want faster quotes, stronger coverage options, higher available limits, and policies that fit the real cost of repairing or rebuilding after a flood. For some homeowners, Neptune Flood may offer a modern private flood insurance path that feels more flexible than a traditional NFIP policy.

That does not mean every homeowner should automatically cancel NFIP. The right decision depends on your property, lender, coverage limit, deductible comfort level, and how the policy responds after a covered flood. If you are searching for flood insurance near me, do not compare by premium alone. A lower annual price can be a poor trade if the policy does not satisfy your mortgage company, excludes property you assumed was covered, or creates a gap between your home’s rebuild cost and the insurance limit.

NFIP remains familiar and widely used. However, many homes now have replacement costs that exceed basic program limits, and many homeowners want to know whether private flood insurance can provide a better match. Neptune Flood is often considered when a homeowner wants a quick online quote, higher available limits, a private-market alternative, or a way to compare flood coverage before a renewal, home closing, or storm season.

Quick facts: NFIP to Neptune Flood comparison

Use this snapshot to understand why homeowners compare NFIP with Neptune Flood. The right choice depends on your address, flood zone, lender requirements, rebuild cost, contents exposure, deductible selection, and policy language.

| Decision point | Why homeowners compare Neptune | What to verify first |

|---|---|---|

| Coverage limits | Private flood policies may offer limits that better match higher-value homes | Building limit, contents limit, other structures, and realistic replacement cost |

| Quote speed | Neptune’s digital quote process may be faster for many eligible properties | Correct address, occupancy, foundation, prior loss, and lender information |

| Policy flexibility | Private flood options may include different deductible and coverage choices | Exclusions, waiting period, claim terms, selected endorsements, and deductible rules |

| Premium comparison | Some homeowners want an alternative when NFIP pricing no longer feels competitive | Total value, not just premium: compare coverage strength against annual cost |

| Lender approval | Private flood may satisfy lender requirements when the policy qualifies and is accepted | Written lender or servicer confirmation before canceling existing coverage |

Why homeowners are switching from NFIP to Neptune Flood

Homeowners usually start comparing Neptune Flood after one of five triggers: a renewal increase, a home purchase, a lender flood requirement, a higher rebuild-cost concern, or a realization that standard flood limits may not match their real exposure. NFIP is still important, but its standardized structure can feel restrictive when a home needs broader limits, different deductible options, or faster private-market handling.

Switch only when the replacement policy provides a stronger overall fit for your building, contents, lender requirement, deductible comfort level, and claim expectations. A cheaper quote is not enough by itself.

NFIP vs Neptune Flood: side-by-side comparison points

NFIP and Neptune Flood address the same broad risk—flood damage—but they operate in different lanes. NFIP is the federal flood insurance program with standardized rules and familiar lender handling. Neptune Flood is a private flood insurance option that may offer different pricing, limits, underwriting, and coverage selections. The best choice depends on the property, not the headline.

| Category | NFIP | Neptune Flood / private flood | Best decision rule |

|---|---|---|---|

| Building limits | Standardized program limits; residential building coverage is commonly capped at $250,000 | May offer higher available limits depending on eligibility, state, and underwriting | Match coverage to realistic rebuild cost and lender requirements |

| Contents coverage | Separate contents limit; residential contents coverage is commonly capped at $100,000 | May provide different contents choices depending on policy terms | Inventory personal property and confirm basement/lower-level rules |

| Waiting period | Typically subject to a 30-day waiting period unless an exception applies | Private waiting periods can differ by state, timing, underwriting, and moratorium rules | Buy before storm season, not when flooding is already forecast |

| Lender familiarity | Widely recognized by mortgage lenders | May be accepted, but the specific policy should be confirmed with the lender | Get lender approval before canceling existing coverage |

| Policy design | More standardized | May offer more flexible private-market design | Read exclusions, endorsements, claim terms, and deductible wording |

Coverage fit: what homeowners should compare before leaving NFIP

The best flood insurance policy is the one that responds the way you expect after a covered flood. Before switching from NFIP to Neptune Flood, compare covered property, excluded property, detached structures, finished basements, crawlspaces, enclosures, personal property, temporary living expenses, debris removal, claim documentation, and how deductibles apply.

| Coverage item | Question to ask | Why it matters |

|---|---|---|

| Building coverage | Does the limit reflect the cost to repair or rebuild damaged covered property? | Loan balance is not the same as rebuild cost |

| Contents | Are personal belongings covered at the level and valuation method you expect? | Flooded contents can create a large uninsured loss |

| Lower levels | How does the policy treat basements, crawlspaces, and enclosed areas? | Many flood claim disputes come from lower-level limitations |

| Temporary housing | Does the policy offer additional living expense or loss-of-use coverage? | Displacement after a flood can be expensive even if repairs are covered |

| Other structures | Are detached garages, sheds, fences, pools, docks, or retaining walls addressed? | Exterior improvements may not be covered the way homeowners assume |

Lender acceptance: the step homeowners cannot skip

If your mortgage requires flood insurance, lender acceptance matters as much as price. Private flood insurance can be a viable option in many situations, but the specific policy must satisfy the lender’s flood insurance requirement. Before canceling NFIP, send the proposed private flood declarations, policy details, and mortgagee clause information to the lender or loan servicer for review.

- The lender accepts the private flood policy for your loan.

- The building limit satisfies the lender’s required amount.

- The effective date does not create a coverage gap.

- The mortgagee clause is correct.

- You have written confirmation before canceling existing coverage.

If you are closing on a property, timing matters. Do not assume the closing team, lender, and insurer are aligned until the final evidence of flood insurance is approved.

When homeowners should not rush the switch

Switching from NFIP to Neptune Flood can make sense, but it should not be rushed. Homeowners with prior flood losses, complex foundations, lender issues, elevation concerns, active claims, properties in coastal surge zones, or planned real estate transactions should compare carefully. The goal is not simply to replace NFIP. The goal is to avoid a costly gap when the next flood happens.

| Situation | Why to slow down | Best next step |

|---|---|---|

| Mortgage-required coverage | The lender must accept the replacement policy | Get approval before canceling NFIP |

| Prior flood claim | Claims history can affect underwriting and eligibility | Disclose prior losses accurately |

| Basement or enclosure | Coverage limitations can differ by policy | Compare policy language for lower levels |

| Home closing soon | Evidence of insurance must satisfy closing requirements | Coordinate lender, title, and insurance timing |

| Storm approaching | Waiting periods and moratoriums may apply | Buy early instead of waiting for a forecast |

Flood insurance comparison support in our licensed states

Blake Insurance Group helps property owners review flood insurance options across our licensed footprint. Flood risk varies by region: desert washes in Arizona and New Mexico, hurricane and storm surge exposure in Florida and the Southeast, river flooding across the Midwest and Plains, and coastal or urban drainage risk in larger metro areas. A strong flood comparison should reflect the property address, not just the state.

| Region | States | Common switch question |

|---|---|---|

| Southwest and West | AZ, CA, NM, TX | Does private flood offer better fit for flash flooding, coastal areas, desert washes, or higher-value homes? |

| Southeast and Mid-Atlantic | AL, FL, GA, NC, SC, VA, WV | How do hurricane rain, storm surge, inland flooding, and lender requirements affect the policy choice? |

| Midwest and Plains | IA, KS, MI, NE, OH, OK, SD | Should homeowners compare NFIP with private flood for river risk, basement exposure, and severe storm runoff? |

| Northeast | NY | Can private flood better address coastal exposure, condo property concerns, or high-value building limits? |

Get a Neptune Flood quote before your NFIP renewal

The best time to compare Neptune Flood is before renewal, before a home closing, or before storm season. Have your current declarations page ready if you already carry flood insurance. Confirm your address, occupancy, foundation type, replacement cost, contents exposure, lender information, and desired deductible. Then compare the private quote against your current NFIP policy by coverage, not just price.

Coverage is not bound until the application is accepted, required information is complete, payment is made when required, and the carrier confirms the effective date.

Switching from NFIP to Neptune Flood FAQs (2026)

Why are homeowners switching from NFIP to Neptune Flood?

Homeowners often compare Neptune Flood because they want faster quotes, different private-market options, potentially higher available limits, flexible deductible choices, or a stronger fit for their property than a standardized NFIP policy.

Is Neptune Flood always better than NFIP?

No. Neptune may be a strong fit for some properties, while NFIP may still be appropriate for others. Compare lender acceptance, limits, deductible, waiting period, exclusions, and claim rules before switching.

Can I cancel NFIP after getting a Neptune Flood quote?

Do not cancel existing NFIP coverage until the private policy is issued, paid when required, effective, and accepted by your lender if your mortgage requires flood insurance.

Does private flood insurance satisfy mortgage requirements?

It may, but the specific policy must be accepted by the lender or loan servicer. Always confirm lender approval before replacing an NFIP policy with a private flood policy.

When should I compare Neptune Flood with NFIP?

Compare before renewal, before closing on a property, before storm season, or whenever your current flood premium, limits, or coverage terms no longer match your property’s risk.

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with Neptune Flood, NFIP, FEMA, or any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Coverage, eligibility, limits, deductibles, exclusions, underwriting rules, lender acceptance, claim handling, waiting periods, moratoriums, and availability vary by property, state, policy, and carrier. Your issued policy governs coverage. This page is general insurance information and not legal, tax, lending, engineering, or claims advice.

Trademarks: Neptune Flood, NFIP, FEMA, and any carrier or program names are trademarks™ or registered® trademarks of their respective owners. Use of these names is for identification and does not imply affiliation or endorsement.

Reviews are loaded from Google when you click “View reviews.”