High Net Worth Home Insurance (2026): Better Rebuild Protection, Broader Valuables Coverage, and Stronger Liability Planning

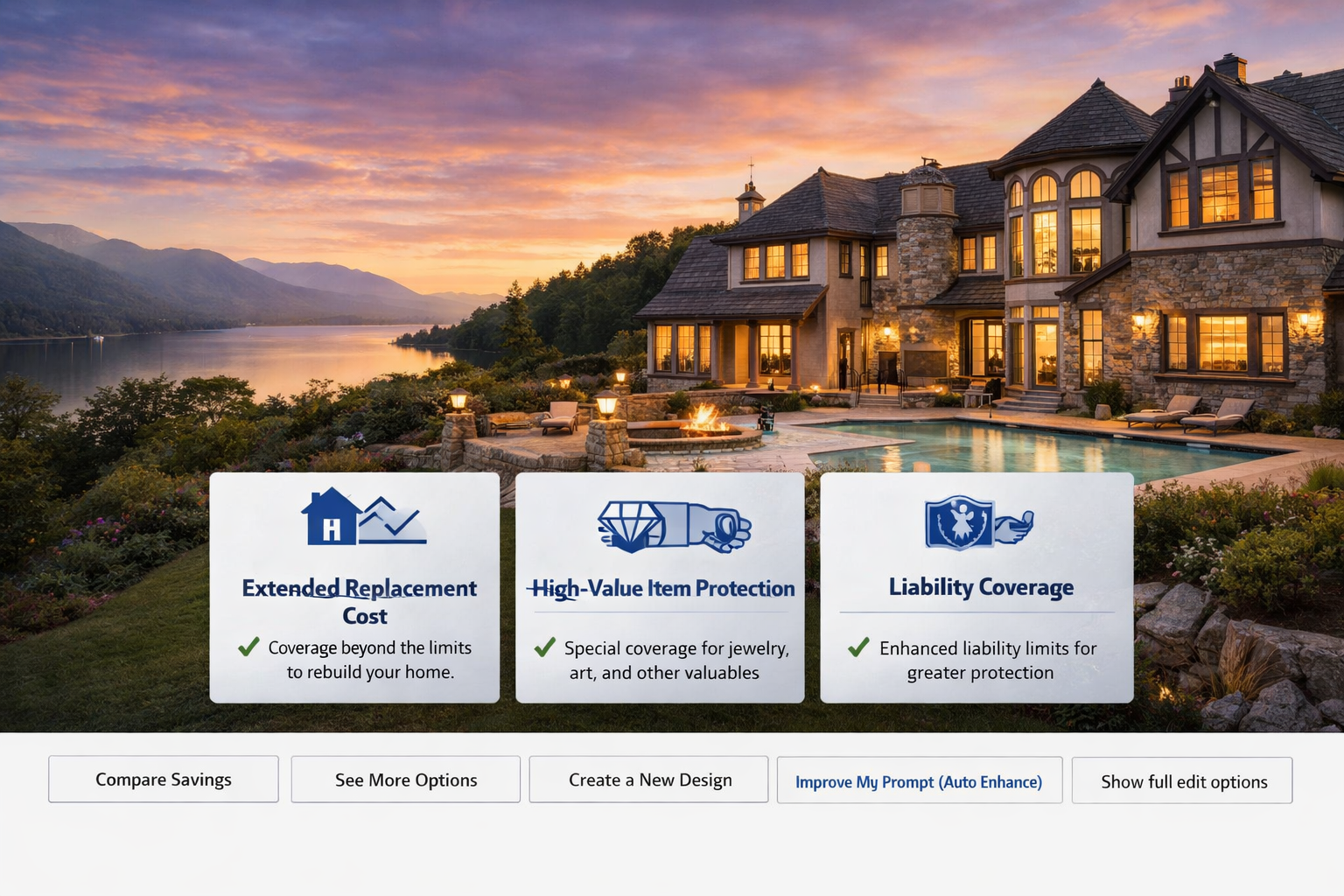

High net worth home insurance is built for households that need more than a standard homeowners policy. If your property has custom construction, premium finishes, detached structures, collectibles, jewelry, wine, art, layered liability exposure, or multiple residences, the cheapest policy is rarely the best policy. The real goal is to protect the full cost to rebuild, preserve lifestyle after a loss, and reduce the chance that a claim reveals a gap you did not know you had.

A luxury home often has a replacement cost that looks very different from its market value. Land value, neighborhood pricing, and real estate appreciation do not tell you what it will cost to reconstruct a custom kitchen, import specialty stone, replace millwork, restore built-ins, or bring damaged portions of the property up to current code. That is why serious home insurance planning starts with a rebuild discussion, not a Zestimate discussion.

The strongest 2026 approach is to review four layers together: dwelling, valuable items, water and catastrophe gaps, and liability/umbrella protection. A high-value home deserves a coordinated protection plan, not a single-line quote in isolation.

Why high net worth home insurance is different from standard homeowners coverage

Standard homeowners vs high net worth home insurance

This table shows the practical differences most households notice first when comparing basic homeowners coverage to a policy designed for higher-value properties.

| Coverage area | Typical standard approach | High-value approach | Why it matters |

|---|---|---|---|

| Dwelling valuation | Broader estimating model, often less tailored to custom finishes | More detailed rebuild focus, sometimes with higher-touch appraisal or risk review | Helps reduce underinsurance when reconstruction costs are complex or unusually high. |

| Personal property | Standard contents limits and tighter category sublimits | Broader planning for high-value contents and more attention to itemized valuables | Important when one room, safe, or collection can represent a major share of household value. |

| Loss settlement | Policy form may be more basic | May offer broader settlement options, including stronger rebuild features on the right form | Loss handling details matter most after a major claim, not before it. |

| Additional living expenses | Useful but often less tailored to luxury lifestyle replacement | Often designed to better support temporary housing at a comparable standard | A long restoration timeline can become a second financial loss without strong loss-of-use protection. |

| Liability strategy | Lower base limits more common | Frequently paired with stronger home liability and a meaningful umbrella | Asset-rich households need lawsuit planning, not just property planning. |

What matters most when you insure a luxury or high-value home in 2026

First, verify the dwelling amount against replacement cost, not purchase price or market value. Second, identify all categories of valuable property that may need scheduling, higher internal limits, or separate handling. Third, review water-related exposures and catastrophe gaps. Standard homeowners policies generally do not cover flood, and many also do not cover earthquake; water backup and similar losses may need specific endorsements or separate protection depending on the carrier and form. Fourth, coordinate your home liability with your auto, recreational exposures, staff exposure, and umbrella liability strategy.

| Item to review | Questions to ask | What strong planning looks like |

|---|---|---|

| Dwelling and other structures | Does the limit reflect custom construction, code upgrades, detached structures, gates, pool houses, walls, and hardscape? | Rebuild values are updated intentionally and not left on autopilot for years. |

| Jewelry, art, and collections | Are there sublimits that are too low? Do specific items need appraisal-based scheduling? | Valuables are documented, reviewed, and protected to a level that matches real exposure. |

| Water and equipment exposure | Is there protection for water backup, hidden water damage, service line issues, or equipment breakdown where needed? | The policy is built around the property’s actual systems and loss history, not generic assumptions. |

| Flood and earthquake gaps | Would a standard homeowners policy leave these exposures uninsured at this location? | Separate protection is considered when geography, topography, or asset concentration justify it. |

| Liability and umbrella | Would the current home liability and umbrella still feel adequate after a serious injury claim or lawsuit? | Underlying limits and umbrella limits are reviewed together, not as separate conversations. |

The right policy is not the one with the lowest premium. It is the one that can absorb a seven-figure reconstruction problem, preserve your household standard of living during repairs, and protect assets if a liability claim reaches beyond ordinary limits.

Common gaps affluent homeowners should close before a claim

The most expensive surprises are usually not the obvious ones. Owners of large or custom homes often discover too late that the dwelling amount was thin, that a major category of valuables had a low sublimit, or that flood, earthquake, sewer backup, or water-main related damage was outside the base policy. Another common issue is umbrella liability that no longer reflects total exposure after a home renovation, a new pool, a second residence, teen drivers, higher public visibility, or meaningful investment growth.

Some high-value carriers also distinguish themselves through broader claims features, stronger rebuild options, risk consulting, or even cash-settlement choices after a covered total loss on the right form. Those features are not universal, so they should be confirmed in writing and matched to the property profile before you rely on them.

What underwriters usually want to see on a high-value home submission

Strong underwriting starts with clean information. Expect questions about roof age and material, electrical, plumbing, HVAC, prior losses, occupancy, security, central station alarms, backup generators, smart leak detection, wildfire or brush exposure where relevant, and whether there are pools, guest houses, short-term rental exposure, household staff, or high-value detached structures. The stronger and more current the property information, the cleaner the market comparison.

Have your current declarations page, rebuild estimate if available, recent appraisals for valuables, roof age, alarm details, and any prior loss information ready.

Get high net worth home insurance quotes that reflect the real property profile

A proper quote should account for custom construction, detached structures, contents quality, valuables, water exposure, liability layering, and separate catastrophe needs where appropriate. That is how you compare policies on substance instead of price alone. For luxury homes, the better buying question is simple: if there is a major loss, will this policy respond the way you expect?

High net worth home insurance FAQs (2026)

What counts as a high net worth home for insurance purposes?

Usually a home with higher reconstruction cost, custom design, premium materials, larger square footage, significant detached structures, or valuable contents and liability exposure that exceed the assumptions of a standard homeowners policy.

Is replacement cost the same as market value?

No. Replacement cost is the amount needed to rebuild with materials of like kind and quality, while market value includes land and local real-estate conditions. For insurance, rebuild cost is the more important number.

Does standard homeowners insurance cover flood damage?

Usually not. Flood is commonly excluded from standard homeowners coverage, which is why many property owners need to consider separate flood protection based on location and risk tolerance.

Do affluent homeowners need umbrella liability?

In many cases, yes. Umbrella liability sits above underlying home and auto liability limits and helps protect savings, property, and future earnings if a major claim or lawsuit exceeds those base limits.

Should jewelry, art, and collections be scheduled separately?

Often yes. Standard policies may have category sublimits that are too low for higher-value items. Scheduling or separately insuring valuables helps align coverage with actual item value and loss exposure.

Independent agency notice: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Policy availability, underwriting, valuation methods, endorsements, separate flood or earthquake options, valuables coverage, and liability limits vary by carrier, state, property, and household profile. Coverage applies only as stated in the issued policy.

Trademarks: Carrier names and product names are the property of their respective owners. Use of them does not imply affiliation or endorsement.