Auto Insurance Review • GEICO Roadside Assistance • 2026

GEICO Roadside Assistance Review (2026): What It Covers, Limits to Watch, Reimbursement Rules, and How to Compare

GEICO roadside assistance can help with towing, jump-starts, tire changes, lockouts, winching, and fuel delivery. This 2026 guide explains what the benefit is designed to do, where limits matter most, and how to compare it with other roadside options before you add it to an auto policy.

For many drivers, roadside help sounds simple until the first real breakdown. That is when the details matter. You do not just want “towing.” You want to know whether the tow goes to the nearest qualified repair facility, whether lockout help has a dollar cap, whether a flat tire service requires a working spare, and whether a stuck vehicle qualifies for winching or turns into an uncovered recovery problem. Those are the details that separate a helpful roadside add-on from a frustrating one.

GEICO’s Emergency Road Service is built to handle common non-accident emergencies. In broad terms, that means the situations most drivers deal with on normal roads: dead battery, flat tire, keys locked in the car, fuel shortage, a vehicle that needs towing after a breakdown, or a vehicle that is stuck on or immediately next to a publicly maintained roadway. It is not designed to be a full mechanical repair plan, and it is not a substitute for understanding the towing and labor limits on your policy.

What is GEICO roadside assistance?

GEICO roadside assistance is usually added to a personal auto policy as Emergency Road Service. In 2026, it remains one of the more straightforward insurer-based roadside options because it focuses on the most common breakdown events rather than trying to bundle travel perks, trip interruption extras, or broad membership benefits. That simplicity is a strength for many households. If you mainly want fast help when the car will not move, a low-cost policy add-on can make more sense than a larger motor club membership.

The trade-off is that insurer roadside benefits are controlled by policy language and practical limits. GEICO publicly describes the core services as towing to the nearest repair facility where repairs can be made, battery jump-starts, tire changes when you have a functioning spare, lockout services up to a stated dollar amount, winching when a vehicle is stuck on or immediately next to a publicly maintained roadway, and fuel delivery. That tells you a lot about fit. This is built for the normal roadside event, not every vehicle problem under the sun.

How roadside assistance usually works in real life

The best time to learn how roadside assistance works is before you need it. In a real breakdown, the experience usually comes down to dispatch method, vendor availability, and the limits on your endorsement.

1) Coverage is tied to the vehicle

Roadside assistance is usually added to a specific vehicle on the policy, not automatically to every car in the household. That matters for families with older second vehicles, commuter cars, or occasional-use vehicles that may not all need the same treatment.

2) You request help through GEICO’s workflow

GEICO directs many roadside requests through its mobile app or online request process, with phone support also available. The mobile workflow is designed to speed dispatch and use your location data to help pinpoint the vehicle.

3) A service vendor is dispatched

Like most carriers, GEICO relies on contracted roadside and towing providers. Response time depends on weather, location, demand, and whether the issue needs a standard tow truck or more specialized equipment.

4) Limits apply at the scene

The service is usually covered only within policy terms. If your vehicle needs more than the covered tow distance, a more expensive recovery setup, parts replacement, or a different destination, you may approve and pay the extra amount yourself.

Practical point: the dispatch workflow can be excellent and the experience can still be disappointing if the policy limit does not match your real driving pattern. Long rural drives and off-route breakdowns expose weak towing terms quickly.

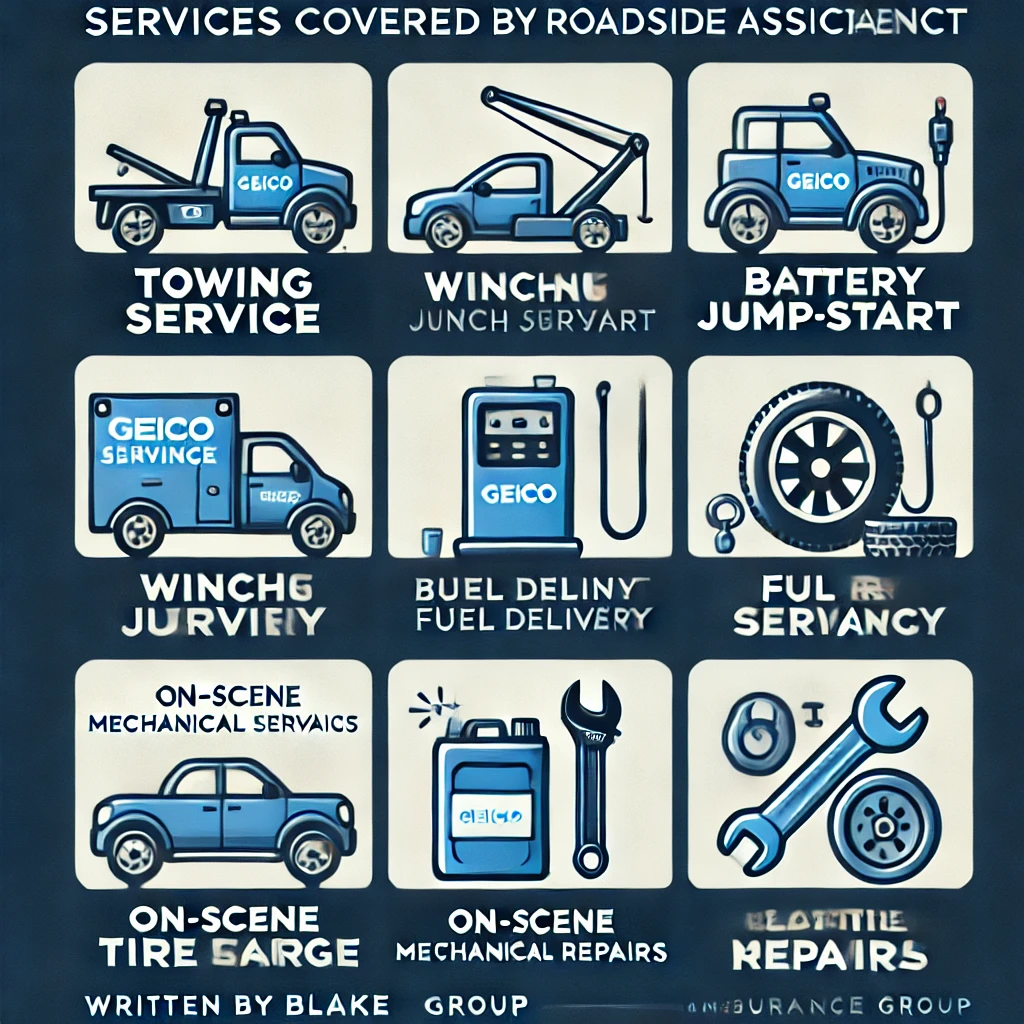

Coverage snapshot: what GEICO roadside assistance typically includes

The categories below align closely with the public-facing GEICO emergency road service description. Your policy wording controls the actual benefit, but this is the right baseline for comparison shopping in 2026.

| Service | What it typically includes | Watchpoints that change the outcome |

|---|---|---|

| Towing | Towing to the nearest repair facility where repairs can be made after a non-accident breakdown. | Nearest-facility language, distance limits, destination preference, after-hours charges, and specialty equipment needs. |

| Battery jump-start | A technician attempts to jump a dead battery at the breakdown location. | Battery replacement is separate, and an electrical issue may still lead to towing. |

| Flat tire service | Labor to change a flat tire when you have a functioning spare. | No spare, damaged spare, unsafe roadside position, or specialty equipment can turn a tire event into a tow. |

| Lockout help | Entry assistance when keys are locked in the vehicle. | GEICO publicly notes a lockout limit up to $100; replacement keys and key-fob programming are separate. |

| Fuel delivery | Delivery of fuel to help you reach a gas station or destination. | Service may be included while the cost of fuel itself can still be charged depending on the situation. |

| Winching | Help pulling the vehicle when it is stuck on or immediately next to a publicly maintained roadway. | True off-road recovery, unsafe conditions, remote extraction, or heavy recovery equipment can fall outside normal roadside scope. |

| Option | Best for | Strengths | Trade-offs |

|---|---|---|---|

| Insurance policy add-on | Drivers who want low-cost protection tied to their insured car | Simple billing, straightforward dispatch, usually inexpensive, easy to manage with the policy | Benefits are vehicle based and can be narrower than membership-style options |

| Motor club membership | Frequent travelers and drivers who want benefits that follow the person | May offer higher-tier towing, travel extras, and broader member-based coverage | Costs more and still comes with tier limits and exclusions |

| Credit card or warranty benefit | Drivers who already have a benefit and want to avoid duplicate spending | Can reduce costs if the benefit is already active | Often reimbursement based, more paperwork, and less predictable dispatch support |

Common limits and exclusions that matter in 2026

Roadside assistance is not a repair policy, a body-shop benefit, or a blank check for every towing scenario. It is emergency help inside a defined scope. That sounds obvious, but it is exactly where many drivers get surprised.

Not a parts-and-repairs plan

The service call itself may be covered, but parts are usually not. If the battery is dead because the battery has failed, the jump may be covered while the new battery is your cost.

Non-accident breakdowns are the main target

GEICO’s roadside language is aimed at breakdown scenarios. If the vehicle is disabled after a crash, towing can still be part of the claim process, but that is not the same as using roadside for a routine non-accident event.

State rules can vary

GEICO notes that services may vary by state, and in North Carolina the coverage is referred to as Towing and Labor Coverage. Always read the state-specific wording before assuming the service behaves exactly the same everywhere.

Reimbursement depends on coverage limits

If you pay out of pocket for a covered roadside event, GEICO offers a reimbursement path, but reimbursement is based on the limits of your coverage. That means receipts matter and coverage terms still control the amount.

The cleanest way to think about this benefit is simple: it is designed to get you unstuck, not to make every emergency free and unlimited.

Is GEICO roadside assistance worth it?

For many drivers, yes. GEICO publicly markets the coverage as available for a very low annual cost per car, which is one reason insurer-based roadside remains popular. That low entry cost means you usually do not need to use the benefit many times for it to feel worthwhile. One tow, one lockout, or one battery event can justify the premium quickly.

The real answer depends on your situation. If you already have strong roadside support through a manufacturer warranty, premium credit card, or motor club, adding roadside to your auto policy may be redundant. If you drive an older vehicle, commute daily, travel long highway stretches, or simply want one-call convenience, a policy add-on can be a smart baseline layer of protection.

| Situation | Risk level | Why roadside helps | What to prioritize |

|---|---|---|---|

| Daily commuter | Medium | Lockouts, dead batteries, and tire problems become expensive at the wrong time | Quick dispatch and straightforward towing terms |

| Road trip or highway driver | High | Distance makes towing bills grow fast | Towing language and destination flexibility |

| Older vehicle | High | Breakdown probability is usually higher | Jump-start, tow, and reimbursement clarity |

| New car with active warranty roadside | Low to Medium | You may already have adequate support | Avoid duplicate coverage unless the policy add-on fills a gap |

Breakdown playbook: what to do when you’re stranded

Roadside assistance works best when the first few minutes are handled correctly. That is especially true at night, on a shoulder, or in bad weather.

- Prioritize safety: turn on hazards, move to a safer location if you can, and stay out of traffic.

- Get your location right: use GPS, mile markers, cross streets, or landmarks. Good location data speeds dispatch.

- Describe the problem accurately: flat with a working spare is different from flat with no spare, and both are different from overheating or being stuck.

- Ask destination questions early: if towing is needed, confirm whether the benefit goes to the nearest qualified repair facility or whether you can choose a different shop.

- Save receipts if you self-pay: GEICO offers roadside reimbursement for covered events, but reimbursement is tied to policy limits, so receipts and details matter.

Where Blake Insurance Group can help

We do not dispatch tow trucks, but we do help drivers compare policy options, explain roadside limits in plain English, and decide whether a roadside add-on belongs on the auto policy or whether another roadside option is a better fit.

| Region | Examples of licensed states | What we optimize for |

|---|---|---|

| Southwest & West | AZ, NM, CA | Coverage fit, heat-related breakdown planning, and long-distance towing questions |

| South & Southeast | TX, AL, FL, GA, SC | Commuter-friendly pricing and practical roadside add-on comparisons |

| Midwest & Plains | OH, IA, KS, NE, SD | Winter readiness, older vehicle planning, and rural towing scenarios |

| East & Mid-Atlantic | NY, NC, VA, WV, MI, OK | Multi-vehicle household comparisons and policy-structure decisions |

If you want a quick benchmark, compare a quote with roadside assistance, a quote without it, and then stack that against any warranty or card benefit you already have. That side-by-side view makes the right answer obvious fast.

GEICO roadside assistance FAQs

How far will towing usually go?

GEICO describes towing as going to the nearest repair facility where repairs can be made. Your endorsement controls the exact limit, so review the policy wording if destination flexibility matters to you.

Does roadside assistance cover locksmiths or new key fobs?

Lockout help is commonly included, and GEICO publicly lists lockout services up to $100. That usually means help getting back into the car, not paying for new keys, fob replacement, or programming.

Can I request help in the app?

Yes. GEICO promotes roadside requests through the GEICO Mobile app and online, with phone support also available. App-based requests can be convenient because location details are easier to pass through.

What if I already paid out of pocket?

GEICO has a roadside reimbursement process, but reimbursement is based on your coverage limits. Keep the original bill and service details so you can submit a proper request.

Is winching the same as off-road recovery?

No. GEICO’s public wording describes winching when the vehicle is stuck on or immediately next to a publicly maintained roadway. That is narrower than broad off-road recovery.

Should I rely on roadside assistance from my credit card?

Sometimes, but compare it carefully. Card benefits can be useful, yet many are reimbursement based and may be less convenient than a policy add-on with direct dispatch support.

Related topics

Independent agency: Blake Insurance Group LLC is an independent insurance agency and is not affiliated with any single insurance company.

Licensing: Licensed insurance producer (NPN 16944666).

Important: Roadside assistance availability, pricing, dispatch methods, limits, and exclusions vary by state, vehicle, and insurer and can change. Your policy documents and endorsements control coverage.

Trademarks: GEICO® and related marks are trademarks of their respective owners. Use of them does not imply affiliation or endorsement.