✔ Licensed Insurance Agents★ Access to A-Rated & A+ Rated Insurance Companies🔒 Secure & Private Online Quotes✓ No Spam✓ We Never Sell Your Personal Information

Medicare Comparison • BCBS vs Mutual of Omaha • 2026

BCBS vs Mutual of Omaha: Medicare Plans, Differences & How to Choose (2026)

Compare BCBS Medicare Advantage options with Mutual of Omaha’s Medigap and Part D approach, including networks, cost structure, enrollment timing, and 2026 decision tips.

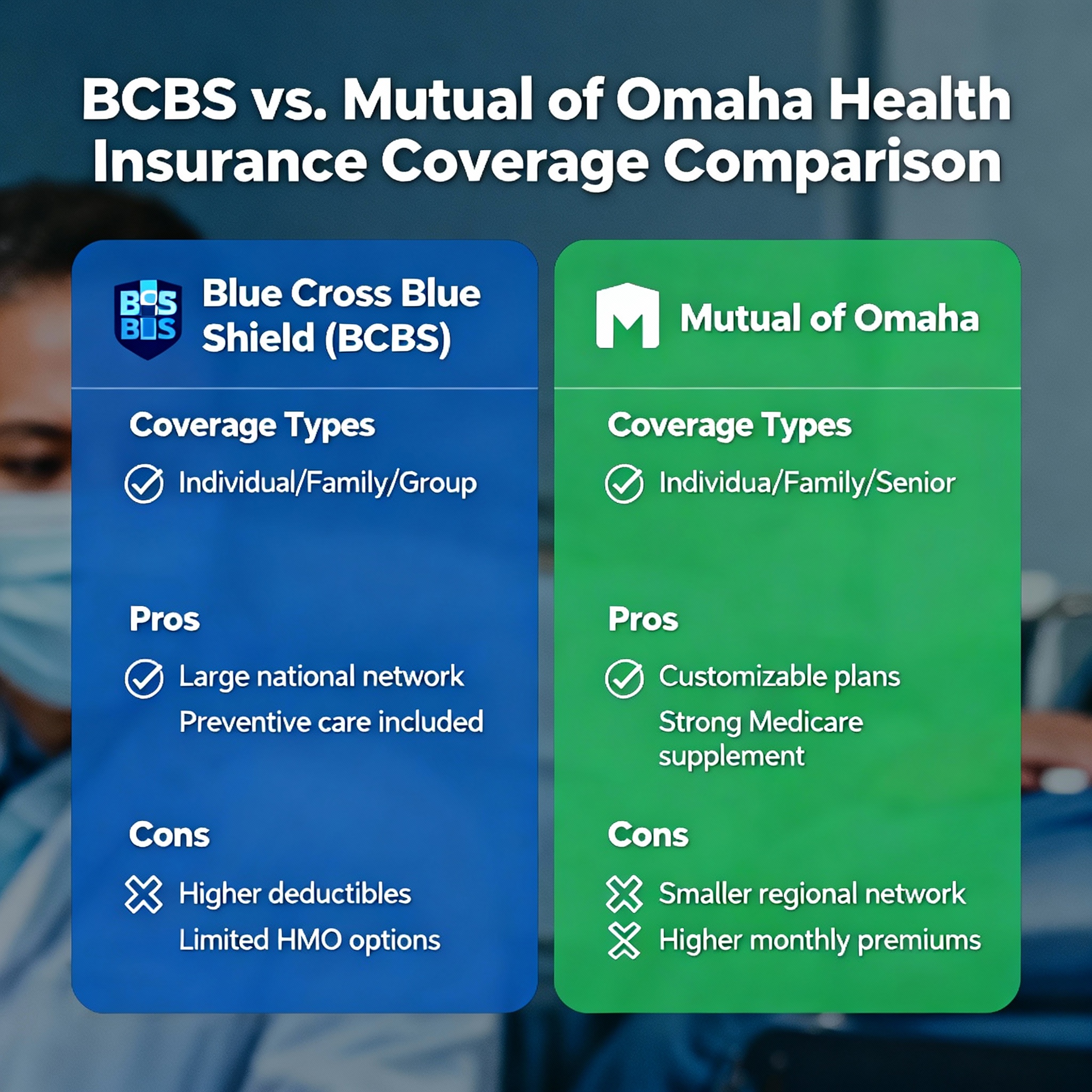

Comparing BCBS vs Mutual of Omaha for Medicare is really a comparison of two different coverage strategies.

Many BCBS-branded Medicare offerings in a given county focus on Medicare Advantage (Part C) with HMO/PPO networks and bundled extras.

Mutual of Omaha is widely known for a Medicare Supplement (Medigap) approach—often paired with a standalone Part D drug plan—where the goal is predictable cost and broad provider freedom.

The “best” choice depends on four things: your doctors, your prescriptions, your travel habits, and your budget style (lowest premium vs most predictable out-of-pocket).

Here’s the simplest way to think about it for 2026: Medicare Advantage can be a great fit if you want an all-in-one plan with extras and you’re comfortable staying in-network.

Medigap can be the better fit if you want maximum provider access and you prefer fewer surprise bills during care.

We’ll walk you through the tradeoffs, then give you two straightforward next steps: shop BCBS options directly, or get independent help across both strategies.

Compare plans the right way: doctors + meds + total cost

Important nuance: “BCBS” isn’t one single plan nationwide. Blue plans are offered by local/state Blue companies, so benefits and networks differ by county.

Mutual of Omaha’s Medigap benefits are standardized by plan letter, but premiums still vary by age, ZIP, and underwriting class.

Coverage & plan differences

BCBS Medicare Advantage (Part C)

Medicare Advantage plans bundle Part A and Part B through a private insurer approved by Medicare. Many plans also include Part D drug coverage (MAPD).

Expect an HMO or PPO network, defined copays/coinsurance, and an annual out-of-pocket maximum for Part A and Part B services.

Many Advantage plans include popular extras (dental, vision, hearing, OTC, fitness) but require you to follow plan rules and stay in network for best pricing.

Mutual of Omaha Medigap (Supplement)

Medigap works alongside Original Medicare to reduce your share of costs. Instead of a network, you typically can see any provider nationwide who accepts Medicare.

Many people pick Medigap for predictable cost sharing and travel flexibility, then add a standalone Part D plan for prescriptions.

Plan G and Plan N are common comparison points: Plan N may trade some copays for lower premiums, while Plan G is often chosen for richer coverage.

Decision area

BCBS Medicare Advantage

Mutual of Omaha Medigap (G/N) + Part D

What it means for you

Doctors & hospitals

In-network focus (HMO/PPO). Referrals/prior auth may apply depending on plan

Any Medicare-accepting provider. No referrals

Advantage = manage network rules; Medigap = maximum freedom

Drug coverage

Usually included (MAPD), but formulary/pharmacy rules still matter

Choose a standalone Part D plan tailored to your medications

Run your meds and pharmacies first to avoid surprises

Monthly premium vs bills

Often lower premium; copays/coinsurance during care up to an annual max

Higher premium; typically fewer point-of-care bills for covered services

Premium savings can be offset by frequent care copays

Travel & snowbirds

Emergency/urgent out-of-area; PPOs may be more flexible than HMOs

Nationwide access with Original Medicare

Frequent travelers often favor Medigap predictability

Changes typically available during the annual election window

Medigap may require underwriting if you apply later (outside protected windows)

Timing can reduce future flexibility—choose deliberately

The winning decision is the one that keeps your doctors accessible and your prescription costs stable—without making you choose between “cheap premium” and “surprise bills.”

Pricing drivers & how to find value in 2026

Medicare shopping becomes simple when you build one comparison model: your doctors + your prescriptions + a realistic estimate of how often you use care.

Then you compare annual cost, not just premium. A $0 premium plan can still be expensive if your specialists are out of network or your drugs land on a high-cost tier.

Driver

Why it matters

Pro move

Medication list & pharmacies

Formulary tiers and preferred pharmacies can swing your annual cost dramatically

Run meds first and confirm the pharmacy network before enrolling

Doctors & facilities

Out-of-network exposure can erase premium savings on Advantage plans

Verify providers for Advantage; Medigap offers broad access with Original Medicare

Usage pattern

Frequent care favors predictable cost structures

Ongoing specialist care often leans Medigap; light users may prefer Advantage + extras

Travel

Out-of-area rules differ and can affect follow-up care

Snowbirds should compare PPO flexibility vs Medigap nationwide access

Enrollment timing

Protected windows vs underwriting can shape your future options

Use your best enrollment window to secure the strategy you want long term

A practical decision rule: if you want lowest monthly premium + extras, start with Advantage and verify network access.

If you want maximum provider freedom + predictable spending, start with Medigap and then optimize Part D using your medications.

Enrollment timing that matters (2026)

Medicare rules allow plan changes during defined windows. The exact option that’s best for you can depend on whether you’re brand new to Medicare,

already enrolled in Advantage, or applying for Medigap outside your protected window. This table keeps it simple.

Enrollment window

Who it’s for

What you can do

Annual Election Period (AEP) Oct 15 – Dec 7

Most Medicare beneficiaries

Join, drop, or switch Medicare Advantage and Part D plans (changes effective Jan 1)

Medicare Advantage Open Enrollment Jan 1 – Mar 31

People already enrolled in Medicare Advantage

One change: switch MA plans or return to Original Medicare (and add Part D if needed)

Special Enrollment Period (SEP)

Eligible life events (moving, losing coverage, etc.)

Make changes when you qualify—timing and documentation rules apply

If you’re considering Medigap, your best purchase window is often tied to your initial Medicare eligibility. Outside that, underwriting may apply depending on your state and situation.

Service areas & licensed states

We help Medicare shoppers across our licensed footprint. Availability varies by county and plan service area.

State

Abbrev.

Sample metros

Arizona

AZ

Phoenix, Tucson, Mesa

Alabama

AL

Birmingham, Mobile, Huntsville

Texas

TX

Houston, Dallas, Austin

California

CA

Los Angeles, San Diego, San Jose

New York

NY

NYC, Buffalo, Rochester

Ohio

OH

Columbus, Cleveland, Cincinnati

Florida

FL

Miami, Tampa, Orlando

North Carolina

NC

Charlotte, Raleigh, Greensboro

Virginia

VA

Virginia Beach, Richmond, Norfolk

Georgia

GA

Atlanta, Savannah, Augusta

Oklahoma

OK

Oklahoma City, Tulsa, Norman

New Mexico

NM

Albuquerque, Santa Fe, Las Cruces

Iowa

IA

Des Moines, Cedar Rapids, Davenport

Kansas

KS

Wichita, Overland Park, Topeka

Michigan

MI

Detroit, Grand Rapids, Ann Arbor

Nebraska

NE

Omaha, Lincoln, Bellevue

South Carolina

SC

Charleston, Columbia, Greenville

South Dakota

SD

Sioux Falls, Rapid City

West Virginia

WV

Charleston, Morgantown, Huntington

BCBS vs Mutual of Omaha: FAQ (2026)

Which is cheaper—BCBS Medicare Advantage or Mutual of Omaha Medigap?

Advantage plans often have a lower monthly premium, but you may pay more at point of care through copays and coinsurance.

Medigap usually costs more monthly, but can reduce bills during care. The better value depends on your doctors, prescriptions, and usage.

Can I keep my doctors with both?

Medicare Advantage depends on the plan’s local network. Medigap works with any provider that accepts Medicare.

We verify your providers first so you don’t lose access after enrolling.

Do I need a Part D plan?

If you choose Medigap, you typically add a standalone Part D plan for prescriptions.

Many Medicare Advantage plans include drug coverage, but you still need to confirm formulary tiers and preferred pharmacies.

Can I switch later?

Advantage plan changes are typically available during the annual election window, and there’s also a Medicare Advantage Open Enrollment period for people already enrolled in Advantage.

Switching to Medigap later may require medical underwriting depending on your situation—timing matters.

Is independent help free?

Yes. Our licensed help is free to you. Carriers compensate agents; your premium is the same with or without assistance.

Medicare help: This page is for the 2026 plan year. For official Medicare information, visit Medicare.gov or call 1-800-MEDICARE (TTY: 1-877-486-2048), 24/7.

Independent agency: Blake Insurance Group LLC is an independent insurance agency. We are not affiliated with Medicare or any government agency.

Licensing: Licensed insurance producer (NPN 16944666). Plan availability, benefits, premiums, provider networks, formularies, and cost sharing vary by county and carrier. Your issued policy and enrollment materials govern.

Trademarks: BCBS and Mutual of Omaha marks belong to their respective owners; use does not imply endorsement.

bcbs vs mutual of omaha medicare 2026, blue cross blue shield medicare advantage compare, mutual of omaha medigap plan g vs plan n,

medicare advantage hmo ppo vs medigap, part d drug plan comparison, medicare enrollment periods oct 15 dec 7 jan 1 mar 31,

independent medicare agent near me, snowbird medicare coverage, medicare plan finder compare costs