Need a Florida disability quote?

Protect your paycheck with customized benefit and waiting periods.

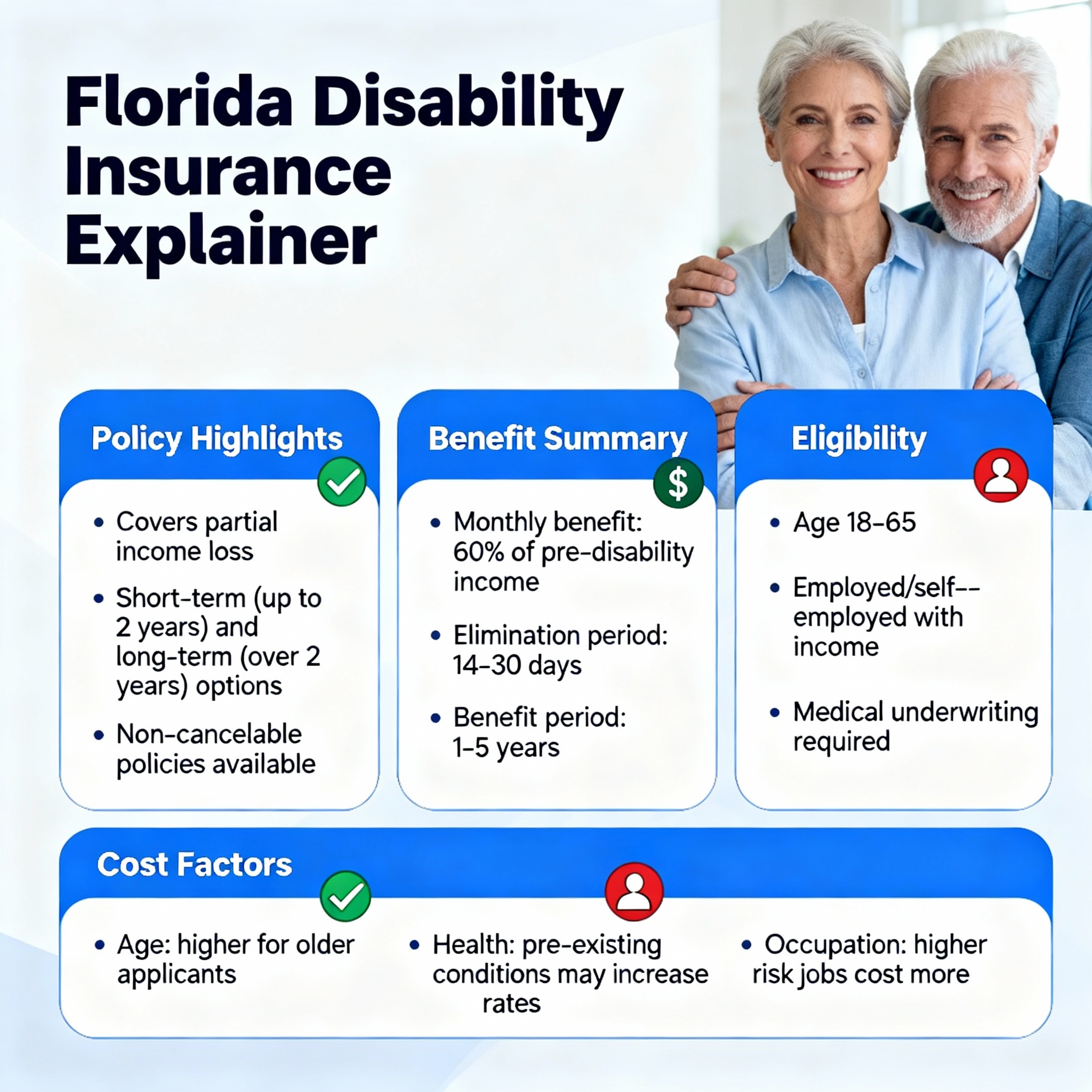

Disability Insurance • Florida (FL) • 2026

Disability Insurance Florida (FL): Income Protection, Waiting Periods & Quote Options

Choosing disability insurance in Florida means protecting your paycheck if illness or injury keeps you from working. This guide breaks down individual vs. group coverage, benefit periods, elimination periods, and riders—plus how underwriting evaluates your occupation and income so you can compare quotes with confidence. If you’re searching for a knowledgeable agent near me, our independent team can help you zero in on the right definition of disability and benefit design for your budget.

Why disability insurance matters

Income security

A disability policy replaces a portion of your income when you can’t work due to a covered sickness or injury, so housing, utilities, and groceries remain funded during recovery.

Own-occupation advantages

“Own-occ” definitions may pay benefits if you can’t perform the substantial duties of your occupation, even if you work in a different job. Definitions vary by carrier and rider.

Custom fit

Set your monthly benefit, elimination (waiting) period, and benefit period around emergency funds and risk tolerance—then refine with riders for partial disability or cost-of-living adjustments.

Portable protection

Individual policies are yours to keep, even if you change employers or become self-employed.

What Florida disability policies can cover

Availability depends on underwriting and state rules. Your final policy controls what’s covered and excluded.

| Feature / Rider | What it helps with | Typical choices |

|---|---|---|

| Monthly Benefit | Replaces a portion of income while disabled. | Often 50–60% of income up to carrier maximums. |

| Elimination Period | Waiting period before benefits start. | 30, 60, 90, 180 days (90 days common for individual DI). |

| Benefit Period | How long benefits can be paid for a claim. | 2 years, 5 years, to age 65/67, or age 70 (varies by product). |

| Own-Occupation Definition | Pays if you can’t do the material duties of your own job. | True own-occ, modified own-occ, or any-occ by policy. |

| Residual/Partial Disability | Benefits for partial loss of income when working part-time. | Often optional rider with minimum loss thresholds. |

| Future Increase Option | Increase benefit later without full medical underwriting. | Trigger windows tied to income changes or anniversaries. |

| Cost of Living Adjustment (COLA) | Increases monthly benefit while on claim. | Fixed % or CPI-linked options (availability varies). |

| Catastrophic Disability Rider | Additional benefit for severe impairments. | Definition and amounts vary by carrier. |

Florida disability insurance cost: key drivers & savings ideas

Premiums reflect age, health, occupation class, benefit design, and riders. The table below highlights the main rating factors and ways to personalize cost without sacrificing critical protections.

| Factor | How it may affect premium | Ways to optimize |

|---|---|---|

| Age & health | Earlier purchase and favorable underwriting can lower cost. | Apply while healthy; complete exam requirements promptly. |

| Occupation class | Higher-risk duties or heavy manual work may rate higher. | Clarify job duties; ask about class upgrades for promotions. |

| Elimination period | Longer waits generally reduce premium. | Coordinate with emergency savings to consider 90–180 days. |

| Benefit period & amount | Longer periods and higher benefits cost more. | Balance “to age 65/67” vs. 5-year benefits based on risk. |

| Riders | COLA, residual, and FIO add cost. | Prioritize residual and FIO; add COLA if budget allows. |

| Discounts | Multi-life, association, or employer-sponsored discounts. | Ask about employer list-bill or professional associations. |

Occupations & underwriting insights

Underwriters consider your day-to-day duties, time spent in office vs. field, licenses, and income documentation. Professionals (medical, legal, accounting), skilled trades, sales, and small business owners may each receive different occupation classes with distinct pricing and benefit options.

- Documentation: Pay stubs, tax returns (for self-employed), job description, and any group DI details.

- Coordination: If you have group DI, individual policies can “top up” to a desired benefit level.

- Stability: Consistent earnings and tenure can support higher benefit eligibility.

How to choose—and get quotes quickly

- Pick your target monthly benefit (what you need to cover essential bills).

- Select an elimination period that aligns with your savings (e.g., 90 or 180 days).

- Choose a benefit period (5 years or to age 65/67) and key riders (residual/FIO, COLA).

- Start a quote below—our team will compare multiple carriers and walk you through tradeoffs.

Service areas & licensing

| Target Cities (FL) | Licensed States |

|---|---|

| Miami, Orlando, Tampa, Jacksonville, St. Petersburg, Hialeah, Fort Lauderdale, Tallahassee, Sarasota, Gainesville | AZ, AL, TX, CA, NY, OH, FL, NC, VA, GA, OK, NM, IA, KS, MI, NE, SC, SD, WV |

Florida disability insurance: FAQ

How much disability insurance can I qualify for?

Carriers typically cap monthly benefits as a percentage of income (often around 50–60%) and may offset group DI. We’ll review pay stubs or tax returns to size benefits accurately.

What’s the difference between short-term and long-term DI?

Short-term DI pays for weeks to months after a brief elimination period; long-term DI is designed for extended disabilities with longer elimination periods and multi-year benefits.

Is own-occupation coverage worth it?

For professionals and skilled workers, own-occ can better protect your specific job duties. We’ll compare true own-occ, modified own-occ, and any-occ definitions by carrier.

Can self-employed Floridians get coverage?

Yes. Individual DI is common for self-employed and small business owners. Income documentation determines eligible monthly benefit and riders like FIO may add future flexibility.

Will my premium increase over time?

Level-premium policies aim for stable pricing; graded options start lower and step up. We’ll show both structures so you can match cash flow and long-term needs.

Independent agency: Blake Insurance Group LLC is an independent insurance agency. We compare multiple carriers and policy options to fit your needs.

Brand ownership: All trademarks and service marks are property of their respective owners. Use here is for identification only; no affiliation or endorsement is implied.

Licensing: Licensed insurance producer (NPN 16944666). See the service area table for state availability: AZ, AL, TX, CA, NY, OH, FL, NC, VA, GA, OK, NM, IA, KS, MI, NE, SC, SD, WV.